A Step-By-Step Guide To A Personal Loan Application

-

- November 11th, 2025

- 3,990 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

We've all faced unexpected expenses, wedding planning, or debt consolidation. Personal Loans often become a go-to solution in such cases, yet navigating its twists and turns can be daunting. This guide alleviates your concerns, offering a step-by-step roadmap to Apply for a Personal Loan Online or offline in India. We've covered you, from preparing your documents to managing your repayments.

Understanding Personal Loans

Types of Personal Loans

Unsecured Loans

● Definition: Unsecured loans are Personal Loans that do not require you to put up any collateral, such as your home or car.

● Interest Rates: Because the lender's risk is higher, the interest rates for personal loans are generally higher than those for secured loans.

● Examples: Credit card loans and most Personal Loans fall under this category.

● Best For Those who need quick funds but don't have any assets to offer as collateral.

Secured Loans

● Definition: Secured loans require you to offer an asset as collateral. This could be your home, car, or investments.

● Interest Rates: Generally come with lower interest rates as the lender has the security of knowing they can seize the asset if you default.

● Examples: Home equity loans and car title loans.

● Best For Those who own a valuable asset and need a larger loan amount.

Fixed-Rate Loans

● Definition: With a fixed-rate loan, the interest rate remains the same throughout the entire term of the loan.

● Interest Rates: Rates are generally higher than the initial rates of a variable loan.

● Examples: Most Personal Loans and home loans offer fixed-rate options.

● Best For Those who want predictable monthly payments and are risk-averse.

Variable-Rate Loans

● Definition: In a variable-rate loan, the interest rate can change at any time, usually in line with a rise or fall in market interest rates.

● Interest Rates: Initial rates are generally lower than fixed-rate loans.

● Examples: Some Personal Loans, most credit cards, and certain home loans.

● Best For Those who are financially secure enough to handle the risk of their monthly payments fluctuating.

When to Consider a Personal Loan

Not every financial crunch warrants a Personal Loan. Knowing when to opt for one can save you unnecessary debt and stress.

● Medical Emergencies: When insurance falls short.

● Debt Consolidation: To pay off multiple debts at a lower interest rate.

● Home Renovation: Enhancing property value.

Suppose you have multiple credit card debts. You can calculate Personal Loan terms to consolidate these debts into a single, manageable repayment plan.

Preparing for the Loan Application

Assessing Your Financial Health

Before you take the plunge, evaluating your financial standing is crucial. Why? Because this will determine your loan eligibility and interest rates.

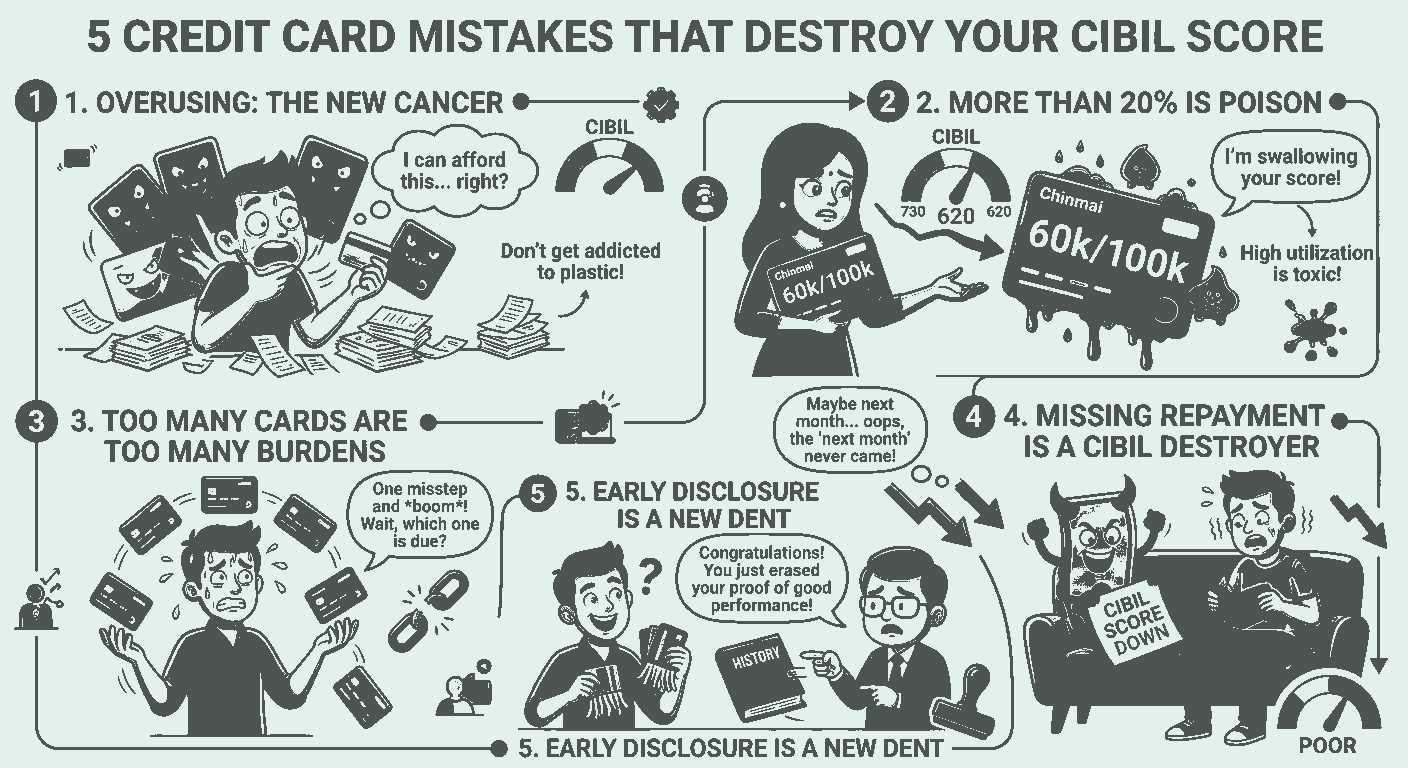

● CIBIL Score: A score above 750 boosts your loan approval chances.

● Debt-to-Income Ratio: Should be below 40% for better loan terms.

Required Documentation

You don't want your loan application to stall due to incomplete paperwork. Here's what you'll generally need:

● Identity Proof: Aadhaar card, PAN card, or Passport.

● Income Proof: Latest salary slips or Income Tax Returns.

Finding the Right Lender

Traditional Banks vs. NBFCs

Your choice of lender can significantly influence your loan experience.

● Traditional Banks: Lower interest rates but stricter eligibility criteria.

● NBFCs: Easier approval but often higher interest rates.

Comparing Interest Rates and Terms

Comparing lenders is more than just looking at interest rates.

● Interest Rates: Shop around for the best rates.

● Processing Fees: Some lenders charge upfront fees.

Let's say you find two lenders: one offers an interest rate of 10%, and another offers 12%. It's not just about the lower rate; consider other terms like repayment flexibility.

The Application Process

Online vs. Offline Application

While traditionalists might prefer a bank visit, the younger generation is inclined to Apply for Personal Loan Online.

● Online Application: Convenient, but ensure the lender's website is secure.

● Offline Application: Time-consuming but offers in-person guidance.

Filling Out the Application Form

The application form is your first official step in the loan process.

● Personal Details: Double-check all entries for accuracy.

● Loan Amount and Tenure: Be realistic about your repayment capacity.

The Verification Process

Once you submit your form and documents, the lender will verify your details.

● Document Verification: Usually takes 24-48 hours.

● Interview: Some lenders may require a personal or phone interview.

After the Application

Loan Approval and Disbursement

After verification, you'll receive a loan agreement detailing the terms.

● Loan Disbursement: This usually occurs within a week.

● Repayment Schedule: Make sure to understand your monthly obligations.

Managing Your Loan

Managing your loan is as crucial as getting one.

● EMIs: Always pay on time to avoid late fees.

● Prepayment: Some loans allow early repayment with minimal penalties.

Conclusion

Managing the intricacies of a personal loan application doesn't have to be a daunting experience.. We are sure this guide will be your companion in this journey, helping you make informed decisions every step of the way.