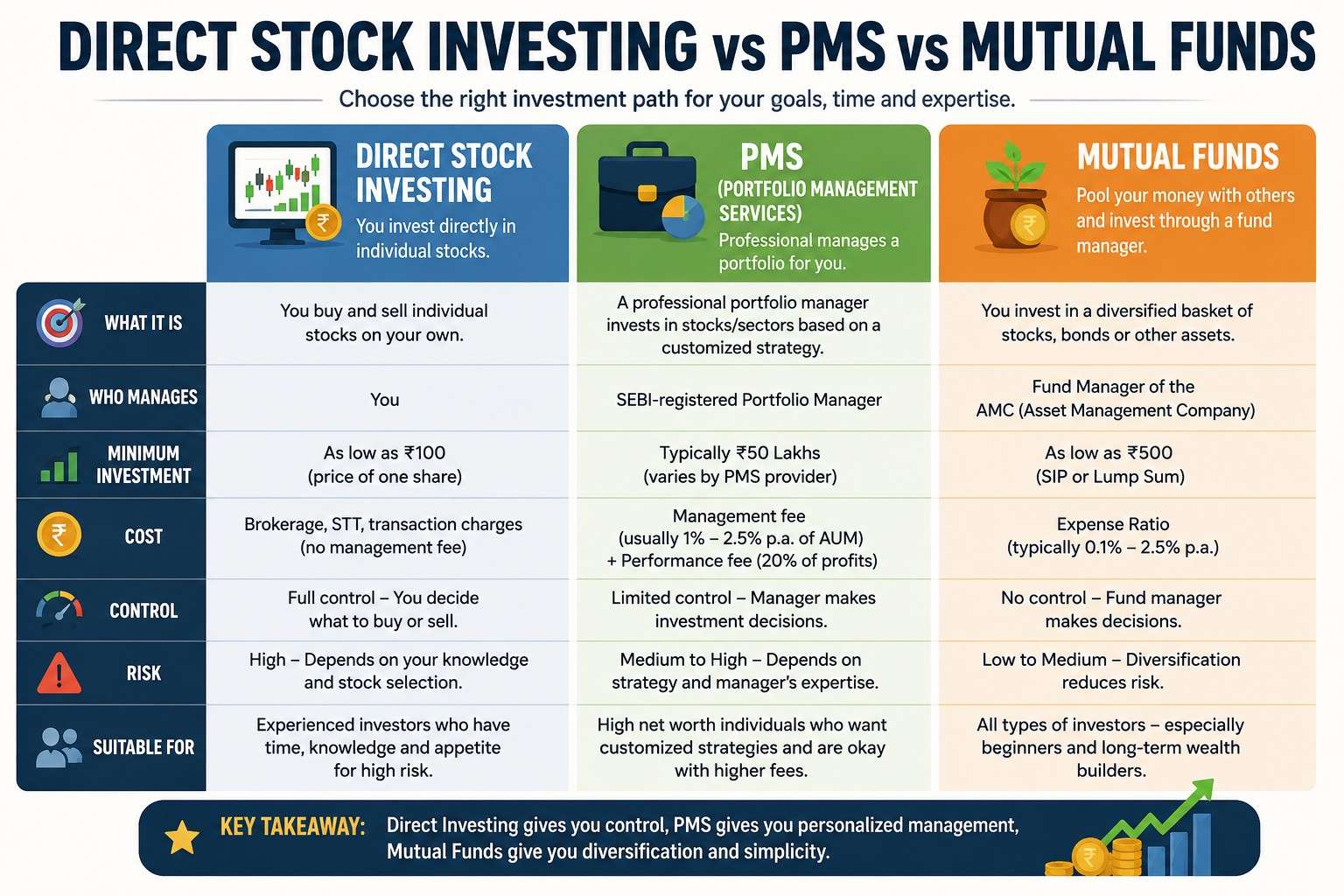

Tax-Free Municipal Bonds: What Investors Need to Know

-

- May 12th, 2026

- 5,117 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

Tax-free municipal bonds are a hidden gem for investors seeking stable income with a side of tax savings. By offering interest that's often exempt from federal, state, and local taxes, these bonds provide a unique opportunity to enhance your returns without the tax bite. But before diving in, it’s crucial to understand how they work, the risks involved, and how they compare to other bonds. Gain insights on municipal bonds through https://zentrix-ai.org, a firm connecting investors to experts who specialize in navigating the nuances of tax-free investments.

The Tax Advantages of Municipal Bonds

When it comes to generating income, tax-free municipal bonds offer a compelling benefit: the interest earned is often exempt from federal taxes. This can be a significant perk, especially for those in higher tax brackets. Think about it—every dollar saved on taxes is a dollar that stays in your pocket.

But that's not the whole story. Depending on where you live, these bonds might also be free from state and local taxes. This double or even triple tax exemption can boost your effective yield, making municipal bonds a smart choice for tax-conscious investors.

For example, if you're living in New York and invest in a New York municipal bond, you could potentially avoid federal, state, and city taxes on your earnings. This can turn a modest yield into a much more attractive return.

However, there’s a bit of fine print. Not all municipal bonds are created equal. Some, known as Private Activity Bonds (PABs), could be subject to the Alternative Minimum Tax (AMT).

This is a separate tax system that runs parallel to the regular tax system, and it could reduce the tax benefits of certain bonds. So, it’s wise to consult with a tax advisor to see how these bonds fit into your overall tax strategy. You wouldn’t want to be surprised come tax time!

Assessing the Risk Profile of Municipal Bonds

Investing in municipal bonds might sound like a safe bet, and often it is. But like any investment, it’s important to weigh the risks. One of the primary concerns is credit risk, which is essentially the chance that the bond issuer might default on their payments.

While most municipal bonds are considered safe, not all are created equal. Some municipalities are in better financial shape than others. For example, bonds issued by a thriving city are generally less risky than those from a struggling town. So, it’s crucial to do your homework.

Interest rate risk is another factor to consider. Simply put, if interest rates rise, the value of existing bonds typically falls.

Imagine holding a bond that pays 3% when new bonds are offering 5%. Suddenly, your bond isn’t looking so hot, right? This is why some investors prefer short-term bonds in uncertain interest rate environments.

Finally, market risk plays a role. Municipal bonds can be less liquid than other types of investments, meaning they might be harder to sell quickly at a good price. Think of it like trying to sell a house in a slow market—you might have to wait a while or accept a lower offer. For this reason, it's essential to consider your time horizon and liquidity needs before diving in.

Comparing Tax-Free Municipal Bonds to Taxable Bonds

So, what's the big deal between tax-free and taxable bonds? At first glance, taxable bonds often offer higher yields. But don’t let that fool you. When you factor in the tax benefits of municipal bonds, the scales might tip in favor of the tax-free option. Let's break it down with an example.

Imagine you’re considering two bonds: one is a taxable bond with a 5% yield, and the other is a municipal bond with a 3.5% yield. On the surface, the taxable bond looks better, right? But after taxes, the story changes. If you're in a 32% federal tax bracket, that 5% yield shrinks to about 3.4%.

Suddenly, the tax-free municipal bond is looking much more attractive. This is where the concept of the tax-equivalent yield comes into play—it's a handy calculation to determine which bond is truly giving you more bang for your buck.

But it’s not just about taxes. Taxable bonds come in a wider variety, offering exposure to different sectors and credit qualities, which can be an advantage for diversifying your portfolio. On the other hand, municipal bonds tend to be safer, particularly those backed by government entities. They also contribute to community development, funding things like schools, hospitals, and infrastructure projects.

Conclusion

Investing in tax-free municipal bonds can be a smart move, especially if you're looking to keep more of your earnings. While they come with their own set of risks and considerations, understanding the landscape can lead to wise choices that align with your financial goals. Always remember, consulting with a financial expert can help you navigate these options and make the most of your investment strategy.