Debt Management Plan Guide: Loans, Credit, and Smart Repayment Strategies

-

- June 26th, 2026

- 284 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

Understanding how to build a focused debt management plan starts with clear priorities: reduce high-cost interest, protect credit, and keep monthly obligations sustainable. This guide explains loans, credit impacts, and practical repayment techniques that can be applied in most financial situations. The primary keyword appears early: a debt management plan should balance short-term relief and long-term cost reduction.

- Define goals: lower interest, protect credit score, free cash flow.

- Choose a framework (ACE Repayment Framework) to assess and act.

- Compare strategies: avalanche, snowball, consolidation — weigh pros and cons.

- Use budgeting, negotiation, and targeted payments to execute the plan.

Debt Management Plan: Core Principles

What counts as debt and how loans differ

Loans include installment debt (mortgages, auto loans, student loans) and revolving credit (credit cards, lines of credit). Interest structure, tax treatment, and collateral affect priority: secured loans often have lower rates but consequence of repossession or foreclosure. Unsecured consumer debts typically carry higher rates and different legal protections under federal and state law. Credit reports and scores—managed by bureaus such as Equifax, Experian, and TransUnion—drive future loan pricing and options.

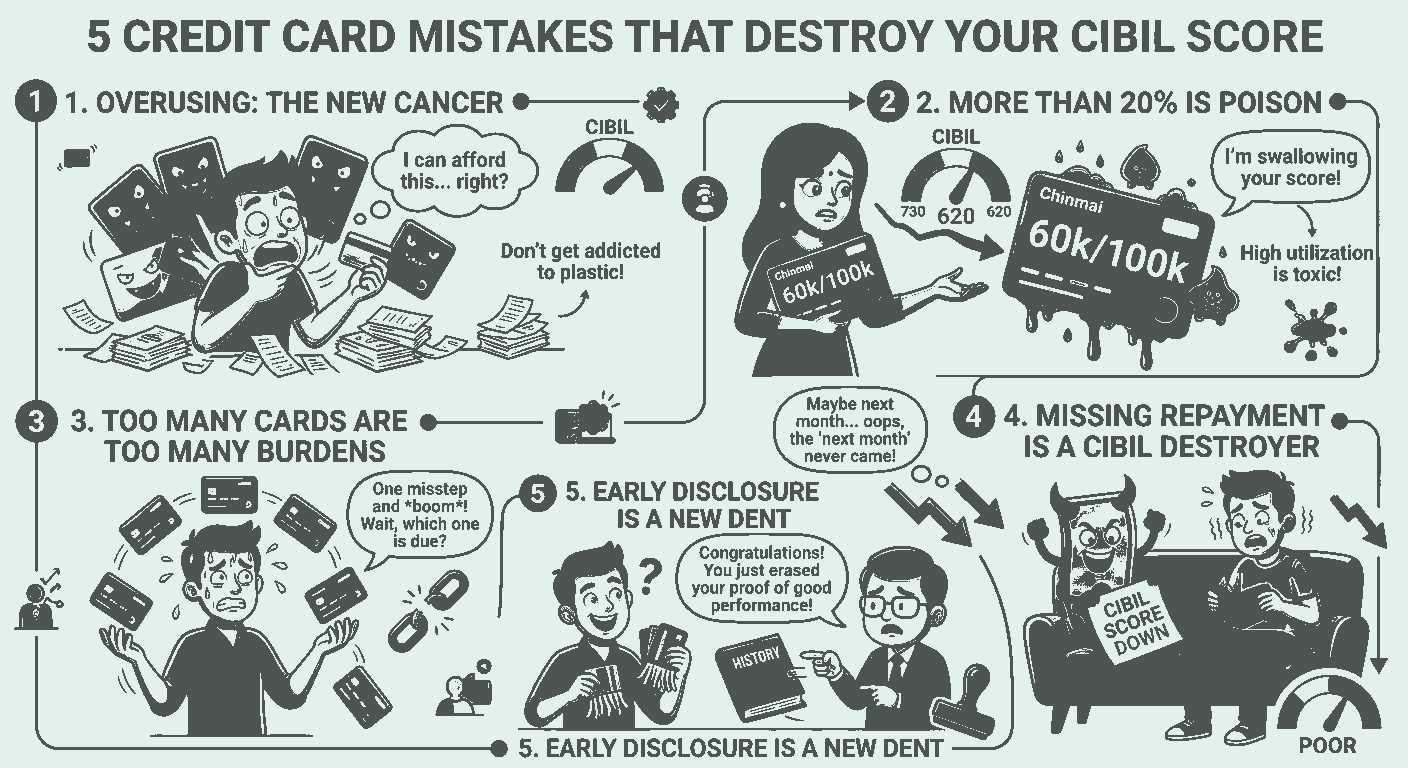

How credit utilization and behavior affect options

Credit utilization tips matter: maintaining utilization below 30% (and ideally under 10% on individual cards) helps credit scores and access to lower-rate refinancing. On the policy side, guidance from the Consumer Financial Protection Bureau and Federal Reserve highlights budgeting and informed borrowing as best practices; see authoritative resources for consumer protections and dispute procedures: Consumer Financial Protection Bureau.

ACE Repayment Framework: A named model to follow

Introduce a concise framework—ACE—to structure execution:

- Assess — inventory debts, interest rates, minimum payments, and legal terms.

- Consolidate/Compare — evaluate consolidation, balance transfers, or refinancing against current costs and credit effects.

- Execute — select a repayment strategy, set automatic payments, and monitor progress.

ACE Repayment Checklist

- List each creditor, balance, APR, minimum payment, due date.

- Calculate total monthly debt service and percentage of net income.

- Prioritize high APR debts and immediate risks (late fees, repossession).

- Check prepayment penalties or loan-specific rules.

- Set a target payoff date and automate payments.

Loan repayment strategies: practical options

Common strategies explained

Two widely used methods are the avalanche and the snowball. Avalanche focuses on highest APR first to minimize total interest (best for loan repayment strategies motivated by cost). Snowball targets smallest balances first to build momentum and improve adherence. Another option is consolidation—combining balances into one loan or transfer—but assess the debt consolidation pros and cons: lower monthly payments may extend term and increase total interest.

When to consider consolidation or refinancing

Refinancing can reduce APR for fixed-rate installment loans when credit or market rates improve. Balance-transfer cards or personal loans can consolidate credit card debt but often include fees and promotional periods. Use the ACE framework's Compare step and account for impact on credit utilization and scores before executing.

Real-world example: applying the ACE framework

Scenario: A borrower has $12,000 in credit card debt at 18% APR and $20,000 in student loans at 4% APR. Minimum payments are $240 (cards) and $200 (student). Total monthly debt service is $440.

Assess: High-cost credit card interest is the priority. Compare: A personal loan at 9% or a balance-transfer with a 3% fee could lower interest compared to 18% if repayment happens before the transfer promotion ends. Execute: Allocate extra cashflow to credit card balance (avalanche), automate payments, and aim to pay cards off in 18 months. Result: Interest expense drops and credit utilization falls, improving credit score and options for future refinancing.

Practical tips for faster, safer repayment

- Automate payments to avoid late fees and protect credit history.

- Apply extra payments directly to principal on high-APR accounts when possible.

- Negotiate interest rate reductions or hardship accommodations with lenders—document calls and confirmations.

- Use biweekly payments to reduce interest for installment loans without significantly increasing monthly burden.

- Keep an emergency fund (even a small buffer) to prevent new high-cost borrowing during repayment.

Common mistakes and trade-offs

Trade-offs are unavoidable. Lowering monthly payments via consolidation can improve cash flow but may lengthen repayment and increase total interest. Paying smallest balances first (snowball) sacrifices some interest savings for behavioral gains—useful if motivation tends to wane.

Common mistakes

- Ignoring loan terms: prepayment penalties, variable rates, and co-signer exposure.

- Overleveraging after consolidation—opening new credit lines immediately undermines progress.

- Failing to update budget: missed adjustments in income or expenses can derail payment plans.

Monitoring progress and when to change course

Track balances monthly, note changes in interest rates, and adjust the ACE plan if circumstances change. For significant financial distress, contact a nonprofit credit counseling agency or review official guidance from consumer protection organizations.

FAQ: common questions

What is a debt management plan and when should it be used?

A debt management plan is a structured approach to repaying debts through prioritized payments, consolidation, or negotiated terms. Use it when balances, interest, or payment schedules threaten financial stability or when a clear plan will improve long-term costs and credit access.

Which loan repayment strategies reduce total interest most effectively?

The avalanche method reduces total interest fastest by targeting the highest-APR debt first; refinancing high-rate balances into lower-rate loans can also lower interest but requires careful fee and term comparison.

How does credit utilization affect repayment options?

Lower utilization improves credit scores, which can unlock lower-rate refinancing offers and better terms for consolidation. Aim to reduce revolving balances and keep individual card utilization low to maximize benefits.

When is debt consolidation beneficial versus harmful?

Consolidation helps when it reduces the average APR or simplifies payments without significantly extending the repayment term. It is harmful if fees and extended terms increase total cost or if it encourages continued high spending on cleared accounts.

How to get professional help safely?

Seek nonprofit credit counseling or consult regulated financial advisors. Verify credentials and watch for upfront fees or guarantees that sound too good to be true. Official consumer protection resources provide guidance on selecting reputable services.