FD vs Arbitrage Funds: Returns, Tax, and Risk Compared

-

- June 26th, 2026

- 268 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

Understanding the Mechanics of Both Worlds

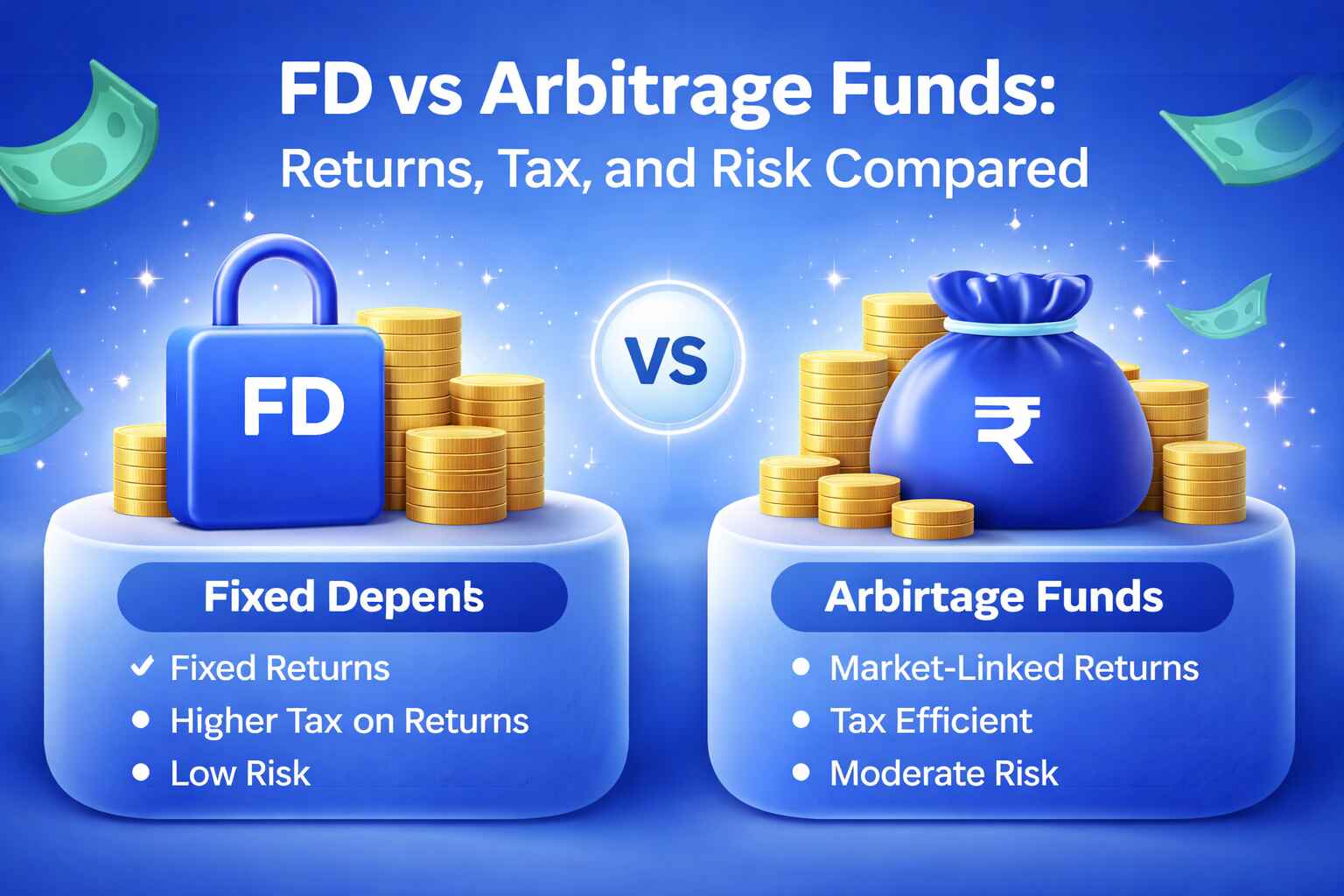

To compare these two, we first need to understand that they are fundamentally different beasts. A Fixed Deposit is a debt instrument. You lend money to a bank, and they promise to pay you a specific interest rate over a fixed period. It is a contract. Whether the stock market crashes or zooms to the moon, your FD interest remains the same. Arbitrage funds, however, are equity-oriented mutual funds. Now, don't let the word equity scare you. They don't bet on whether a stock will go up or down. Instead, they exploit the price difference (the spread) of the same stock in two different markets, usually the cash market and the futures market. For example, if Reliance is trading at ₹2,500 in the cash market but the one-month future is at ₹2,515, the fund manager buys the stock and simultaneously sells the future. They have locked in that ₹15 profit regardless of where the price goes by expiry. Because they are always hedged (buying and selling at the same time), the risk of losing your principal is incredibly low, similar to a debt fund, even though they are technically equity funds.

Comparing the Risk Profiles

When we talk about risk, FDs are the gold standard for safety in India. They are backed by the bank’s balance sheet and insured up to ₹5 lakh by the DICGC. For most people, an FD is as close to risk-free as it gets. Arbitrage funds are also low-risk, but they aren't no-risk. Their risk isn't about the market crashing; it’s about the spread disappearing. If the market is completely flat and there are no price differences to exploit, the arbitrage fund returns vs FD might look underwhelming. There have been rare months where arbitrage funds have given near-zero or even slightly negative returns when the market lacked volatility. Here is the kicker: Arbitrage funds actually thrive on volatility. When the market is swinging wildly, the price gaps between cash and futures usually widen, allowing fund managers to capture better returns. In contrast, an FD doesn't care about volatility it just hums along at its fixed rate.

The Reality of Returns in 2026

If you look at the current numbers for an FD vs arbitrage fund comparison, you’ll see that bank FDs are offering anywhere between 6.5% to 7.5%, depending on the tenure and the bank. Small finance banks might even go up to 8% or 8.5%. Arbitrage funds typically track short-term money market rates. In a normal market, you can expect them to deliver between 6% and 7.5%. On paper, the FD might look like it has a slight edge or is at least equal. But looking at the gross return is a rookie mistake. What matters is what lands in your bank account after the government takes its share.

The Game Changer: Arbitrage Fund Tax Benefits

This is where the battle is won or lost. The arbitrage fund tax benefits are the primary reason why high-net-worth individuals and corporate treasuries prefer them over FDs. Fixed Deposit interest is treated as Income from Other Sources. This means it is added to your total income and taxed at your slab rate. If you are in the 30% tax bracket (plus surcharge and cess), a 7.5% FD actually gives you a measly 5.25% in hand. To make matters worse, banks deduct TDS (Tax Deducted at Source) if your interest exceeds a certain limit, creating a cash flow hurdle. Arbitrage funds, because they hold more than 65% in equity-related instruments (even if hedged), are taxed as Equity Mutual Funds.

(i). Short-Term Capital Gains (STCG): If you sell before 12 months, you are taxed at 20%.

(ii). Long-Term Capital Gains (LTCG): If you hold for more than 12 months, you are taxed at 12.5% on gains exceeding ₹1.25 lakh per year.

What this really means is that even if the arbitrage fund returns vs FD are identical at a gross level (say both give 7%), the person in the 30% slab keeping their money in an arbitrage fund for a year walks away with significantly more money.

Feature |

Fixed Deposit (FD) |

Arbitrage Fund |

Gross Returns |

Fixed (6.5% - 7.5%) |

Variable (6% - 7.5%) |

Tax Treatment |

Taxed at your slab rate (up to 30%+) |

Equity Tax (12.5% LTCG / 20% STCG) |

TDS |

10% (on interest > ₹40k/50k) |

No TDS for residents |

Risk |

Negligible (Credit risk of bank) |

Low (Spread and Liquidity risk) |

Liquidity |

Penalty on early withdrawal |

High (Redeem anytime; exit load usually 15-30 days) |

Liquidity and Flexibility Needs

Here’s the thing about FDs: they are fixed for a reason. If you book an FD for 1 year and need the money in 4 months, the bank will usually charge a premature withdrawal penalty, often 0.5% to 1% of the interest. You also lose the higher interest rate promised for the longer duration. Arbitrage funds are much more liquid. You can put money in today and take it out in a month. Most funds have a small exit load if you withdraw within 15 to 30 days, but after that, it's free. This makes them an excellent parking lot for money you might need on short notice like a down payment for a house or an upcoming tax liability.

Who Should Choose What

We often get asked which one is better. The truth is, there is no single winner; it depends on your specific situation. If you are a retiree in a 0% or 10% tax bracket, the arbitrage fund tax benefits won't mean much to you. In that case, the certainty of an FD is likely your best bet. You want to know exactly how much will hit your account every month to pay the bills. However, if you are a working professional in the 30% tax bracket, putting short-term savings into an FD is arguably one of the most tax-inefficient moves you can make. For you, the FD vs arbitrage fund comparison almost always tilts toward the fund. You are essentially getting a similar risk profile with a much lighter tax burden.

The Impact of Market Volatility on Spreads

It’s worth noting that arbitrage funds do have dry spells. When the market is in a long, boring sideways grind with very low volume, the spreads (the difference between cash and futures) can shrink. In such times, the returns might dip below what a liquid fund or an FD offers. On the flip side, during periods of high market activity like around budget announcements, elections, or major global shifts arbitrage opportunities explode. Smart investors watch these cycles. If you see the market becoming jittery, it’s often a great time to move idle cash into arbitrage funds to capture those wider spreads.

Recent Regulatory Shifts in 2026

Budget 2026 introduced a few subtle changes that investors should keep an eye on. While the fundamental arbitrage fund tax benefits remain intact (the equity-oriented status), there has been an increase in the Securities Transaction Tax (STT) on futures contracts. What this really means is that the cost of doing business for the fund manager has gone up slightly. While this doesn't break the strategy, it might compress the arbitrage fund returns vs FD by a small margin perhaps 10 to 15 basis points. However, even with this slight increase in internal costs, the tax advantage for high-bracket earners remains so massive that arbitrage funds still come out on top for anyone in the 20% or 30% tax category.

Final Thoughts on Mastering the System

In conclusion, choosing between these two shouldn't be about chasing the highest possible return; it’s about choosing the right tool for the job. Fixed Deposits remain a cornerstone of stability, perfect for those who prioritize absolute certainty or those in lower tax brackets. However, for the tax-conscious investor looking to park surplus funds for 3 to 12 months, the arbitrage fund tax benefits provide a compelling edge that is hard to ignore. By understanding that arbitrage fund returns vs FD are often comparable on a gross basis but vastly different on a net basis, you can stop leaving money on the table. Whether you decide to stick with the traditional comfort of the bank or move toward the strategic efficiency of arbitrage, the key is to stay informed and align your choices with your actual take-home goals. For more detailed insights into optimizing your portfolio and staying ahead of tax changes, feel free to explore the resources at. Your money should work as hard as you do, and sometimes, a small shift in where you park it can make a substantial difference in your wealth over time.