What Is Investing? Beginner-to-Advanced Guide to Investing Basics, Strategies, and Risk

-

- June 25th, 2026

- 284 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

Knowing what is investing helps savers move beyond bank accounts and toward long-term goals like retirement, buying a home, or building wealth. This guide explains core concepts, common asset types, practical frameworks, and realistic trade-offs so readers can make informed investment decisions.

- Investing puts capital into assets expecting future returns while taking risk.

- Main asset classes: stocks, bonds, real estate, cash, and alternative investments.

- Use an evidence-based checklist (INVEST) to set goals, allocate assets, control costs, and review performance.

What Is Investing: A Clear Definition

Investing means committing money or capital to an asset with the expectation of generating income, appreciation, or both. The core trade-off is risk versus return: higher expected returns typically require accepting greater uncertainty.

How investing works: risk, return, and time

Risk and return

Return is what an investment earns (income plus price change). Risk is the variability of those returns. Measuring risk uses volatility, drawdown, and probability of loss. Long time horizons usually reduce the chance of permanent loss for diversified portfolios, but short-term swings remain common.

Why time horizon matters

Long-term goals allow exposure to growth assets like stocks; short-term goals favor cash and short-duration bonds to protect principal and liquidity.

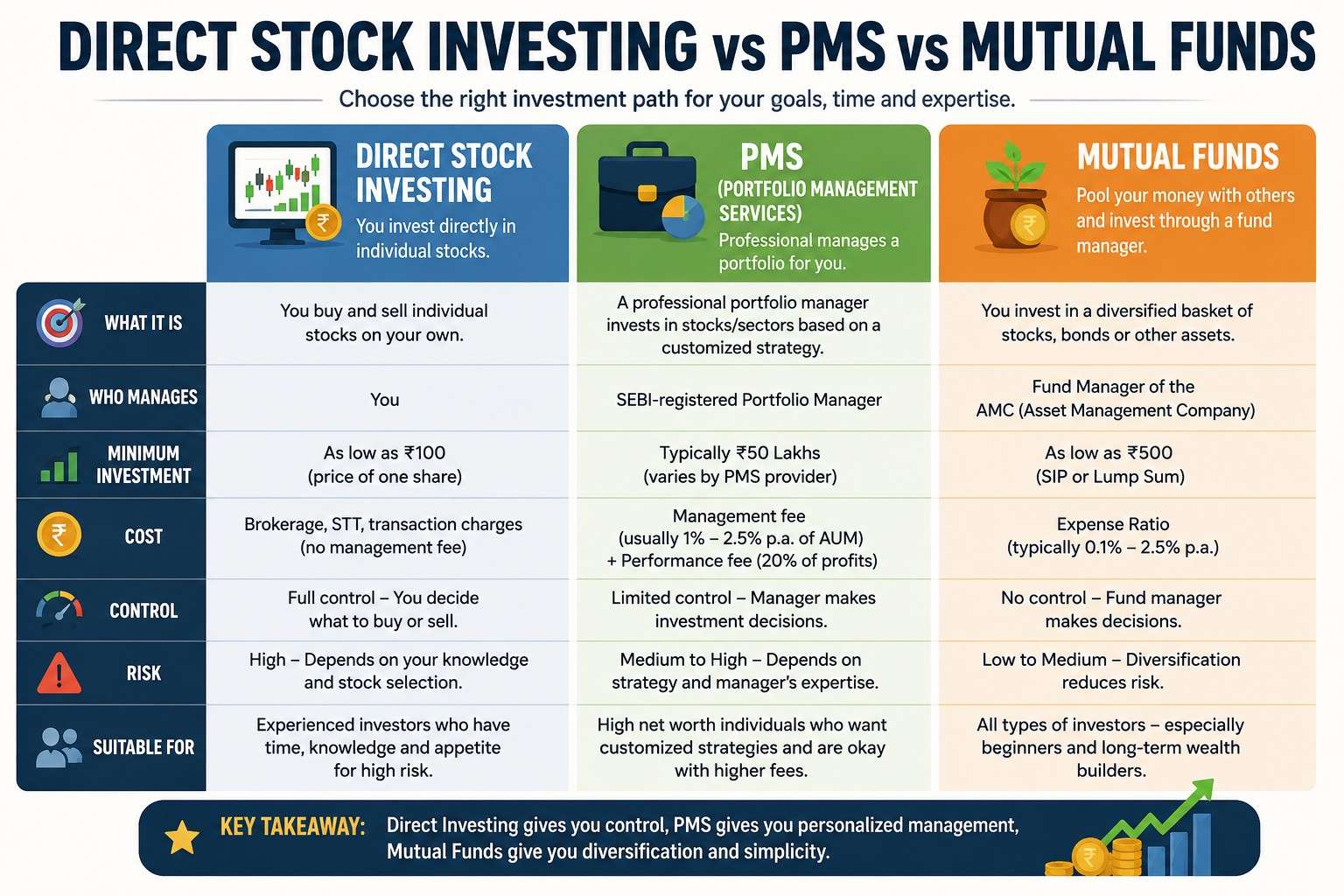

Types of investments (common assets)

- Stocks (equities): ownership in companies; potential for high growth and volatility.

- Bonds (fixed income): loans to issuers; lower volatility and steady income, sensitive to interest rates.

- Real estate: direct property or REITs; provides income and inflation hedge but requires management or liquidity premium.

- Cash and cash equivalents: savings, money market funds; low return, high liquidity.

- Alternatives: commodities, private equity, hedge funds; used for diversification or return enhancement, often less liquid.

Practical investing framework: the INVEST checklist

Use a simple, repeatable framework to make decisions. The INVEST checklist helps organize steps for goals, risk, and execution.

- I — Identify goals: Specify time horizon, target amounts, and purpose (retirement, education, house).

- N — Net position: Calculate net worth, emergency savings, and debt that should be paid down first.

- V — Vehicle selection: Choose account types (tax-advantaged vs. taxable) and investment vehicles (index funds, bonds, ETFs).

- E — Establish allocation: Set asset allocation aligned with risk tolerance and time horizon.

- S — Select low-cost options: Prefer low-fee funds and watch trading costs and taxes.

- T — Test and review: Rebalance periodically and review goals annually or after major life events.

Real-world example

Scenario: A 30-year-old with a 30-year retirement horizon and $6,000 annual savings. After ensuring a 3–6 month emergency fund, the INVEST checklist recommends tax-advantaged retirement accounts, a target asset allocation of 80% equities/20% bonds, low-cost index funds for broad diversification, and an annual rebalance. Over decades, compound returns on that disciplined plan aim to grow savings while managing risk.

Investment strategies for beginners and advanced investors

Strategies for beginners

- Start with a simple diversified mix of low-cost index funds or target-date funds.

- Automate contributions to benefit from dollar-cost averaging.

- Prioritize emergency savings and high-interest debt repayment.

Advanced strategies and considerations

Advanced investors may use tax-loss harvesting, factor tilts (value, momentum), options for income, or alternative allocations. These strategies require deeper knowledge and monitoring and often trade liquidity or simplicity for potential incremental return.

Common mistakes and trade-offs

- Timing the market: Attempting to buy low and sell high often reduces returns due to missed best days.

- Overconcentration: Holding too much of one stock, sector, or country increases idiosyncratic risk.

- Ignoring fees and taxes: High expense ratios and frequent trading can erode returns significantly.

- Chasing performance: Past winners often underperform later; a plan based on asset allocation and rebalancing is more reliable.

Practical tips

- Define one or two clear goals and match assets to time horizons.

- Use tax-advantaged accounts first when available (IRAs, 401(k)s, or country equivalents).

- Prefer broadly diversified, low-cost funds to reduce single-security risk.

- Automate investing with recurring contributions and periodic rebalancing.

- Keep an emergency fund equal to 3–6 months of expenses before taking significant market risk.

For official investor education and protections, see Investor.gov, a resource maintained by the U.S. Securities and Exchange Commission.

Frequently Asked Questions

What is investing and how does it work?

Investing involves allocating money to assets that are expected to generate returns over time. Returns come from income (dividends, interest, rent) and capital appreciation. The process balances expected reward with the risk of loss and uses diversification, asset allocation, and cost management to improve the probability of reaching financial goals.

What are the main types of investments?

Main types include stocks, bonds, real estate, cash equivalents, and alternative investments. Each has different characteristics for return, risk, liquidity, and tax treatment.

How should a beginner start investing with little money?

Open a low-cost brokerage or retirement account, start with diversified index funds or ETFs, automate small recurring contributions, and focus on fees and an emergency fund before taking significant market risk.

How often should a portfolio be reviewed and rebalanced?

Review portfolios at least annually and rebalance when asset allocation deviates significantly from targets (for example, a 5–10% drift) or after major life events.

How does diversification reduce risk?

Diversification spreads exposure across assets that respond differently to market conditions. Combining stocks, bonds, and other asset classes reduces the impact of any single asset's poor performance on the overall portfolio.