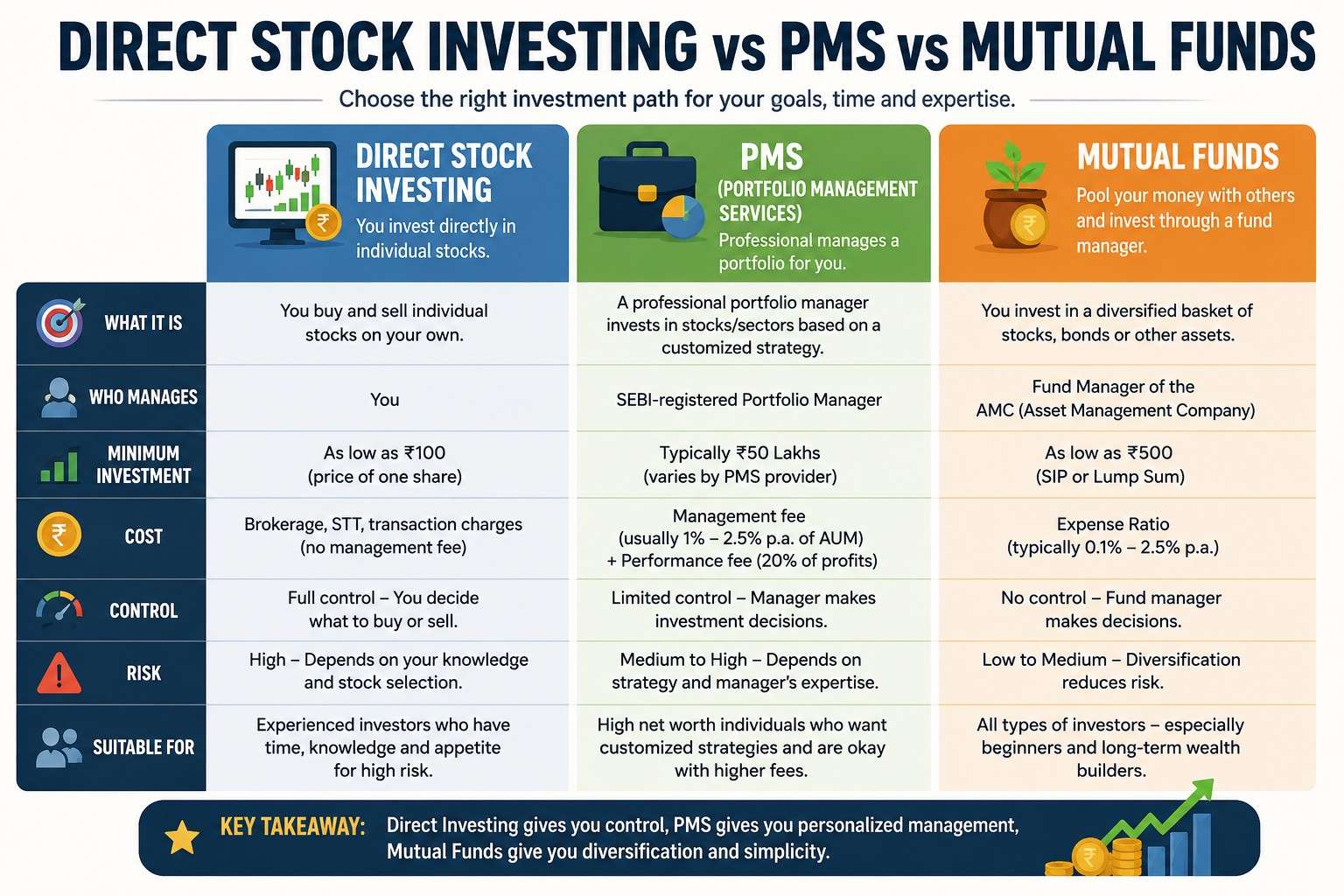

Practical Guide to Investment Risk Fundamentals: Volatility, Diversification & Stability

-

- June 25th, 2026

- 264 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

Understanding investment risk fundamentals starts with clear definitions and practical steps investors can use to protect capital and pursue returns. This guide explains volatility, diversification, stability, and the trade-offs that matter when building or adjusting a portfolio. The term investment risk fundamentals appears here to anchor the key concepts used throughout the article and to guide practical decision-making.

- Volatility measures the variability of returns; risk includes the chance of losing money relative to goals.

- Diversification reduces unsystematic risk by mixing assets with low correlation.

- Stability comes from allocation, time horizon, liquidity, and regular rebalancing.

Investment Risk Fundamentals: definitions that matter

Start with three core terms: volatility (the statistical dispersion of returns, often measured by standard deviation), diversification (combining assets to lower portfolio-level risk), and stability (how consistent portfolio value is relative to goals over time). Related concepts include beta, correlation, drawdown, systematic risk (market-wide) and unsystematic risk (company or sector-specific). Models such as Modern Portfolio Theory (MPT) and measures like the Sharpe ratio provide quantitative context for these fundamentals.

How volatility, diversification, and stability interact

Volatility is an observable property of assets; diversification is an action that changes portfolio volatility and risk exposure; stability is an outcome tied to goals and time frame. For example, adding low-correlation bonds to a stock portfolio commonly reduces overall volatility and potential drawdown, improving short-term stability while affecting expected long-term returns.

Modern Portfolio Theory (MPT) as a framework

MPT offers a model that quantifies the trade-off between expected return and variance of return, seeking an efficient frontier of optimal portfolios. Use MPT as a starting framework to estimate how different allocations change expected volatility and return, while recognizing its assumptions (normal returns, stable correlations) may not hold in stress periods.

STABLE checklist for practical risk control

Use the STABLE checklist when evaluating or redesigning a portfolio:

- S: Stress-test scenarios (market crash, inflation spike)

- T: Time horizon alignment (match investments to goals)

- A: Allocation clarity (target weights by asset class)

- B: Beta and correlation checks (measure systemic vs idiosyncratic risk)

Practical steps to apply these concepts

Follow this concise action plan to make the theory operational: determine risk capacity (how much can be lost without derailing goals), set a target allocation, diversify across low-correlated asset classes, rebalance periodically, and monitor key metrics (standard deviation, maximum drawdown, Sharpe ratio).

Real-world example: a 35-year-old rebalancing plan

Scenario: A 35-year-old with a 20-year retirement horizon holds 80% stocks and 20% bonds. Volatility is high but acceptable given the long horizon. Using the STABLE checklist, this investor maintains an emergency fund (liquidity), stress-tests a 30% drawdown, and rebalances to target allocation annually to capture buy-low sell-high discipline and maintain stability toward the retirement goal.

How to measure volatility and stability

Common metrics: standard deviation (volatility), beta (sensitivity to market), maximum drawdown (largest peak-to-trough loss), and rolling returns (stability over time). Measuring investment stability over time requires rolling-window analysis and attention to correlation shifts during crises: correlations often rise when markets fall, reducing diversification benefits when they are most needed.

Practical tips

- Define goals and time horizons first; risk tolerance is meaningless without objectives.

- Use at least three asset classes (e.g., domestic equity, international equity, fixed income) to start diversification; consider alternatives for added decorrelation.

- Automate periodic rebalancing (quarterly or annually) to enforce discipline and manage drift.

- Keep an emergency cash buffer equal to 3–12 months of expenses to prevent forced selling in downturns.

- Monitor fees and tax impacts—high costs can negate diversification benefits and lower long-term stability.

Trade-offs and common mistakes

Trade-offs: higher expected return usually means higher volatility and the risk of larger short-term losses; more diversification can reduce return if low-return assets dominate; holding too much cash reduces volatility but increases inflation risk. Common mistakes: confusing volatility with permanent loss, over-diversifying into redundant funds, ignoring correlation changes in stress periods, and reacting to short-term volatility with emotionally driven trades.

Practical tools and standards to reference

Use well-documented resources for benchmarks and best practices. For official guidance on diversification basics and investor education, see the U.S. Securities and Exchange Commission's investor pages on diversification and risk management https://www.investor.gov/introduction-investing/why-diversification-matters. Financial professionals often use portfolio analytics platforms and industry standards from bodies such as the CFA Institute when measuring risk-adjusted performance.

When to seek guidance

Consider professional advice when goals are complex (estate, business liquidity needs, tax optimization), when liability matching is required, or when emotional decision-making leads to frequent portfolio changes. Use advisors who explain assumptions and offer stress-test scenarios rather than promising performance.

FAQ: What are investment risk fundamentals and why do they matter?

Investment risk fundamentals are the core concepts—volatility, diversification, and stability—that define how a portfolio behaves under different conditions. They matter because understanding them enables decisions that align risk with financial goals rather than reacting to market noise.

How is volatility different from risk?

Volatility is a statistical measure of return variability; risk is the chance that investment outcomes will prevent reaching financial goals. Volatility contributes to risk but is not the only factor.

How does diversification reduce risk in a portfolio?

Diversification reduces unsystematic risk by combining assets with low or negative correlations so that losses in one holding are offset by gains or smaller losses in others, lowering portfolio variance.

How often should portfolios be rebalanced to manage risk?

Common rebalancing intervals are quarterly or annually; the optimal frequency depends on tax considerations, trading costs, and how quickly allocations drift from targets.

Which volatility measures are most useful for long-term investors?

Standard deviation, maximum drawdown, and rolling returns offer complementary views. Use standard deviation to compare expected variability, drawdown to understand worst-case historical loss, and rolling returns to assess stability over time.