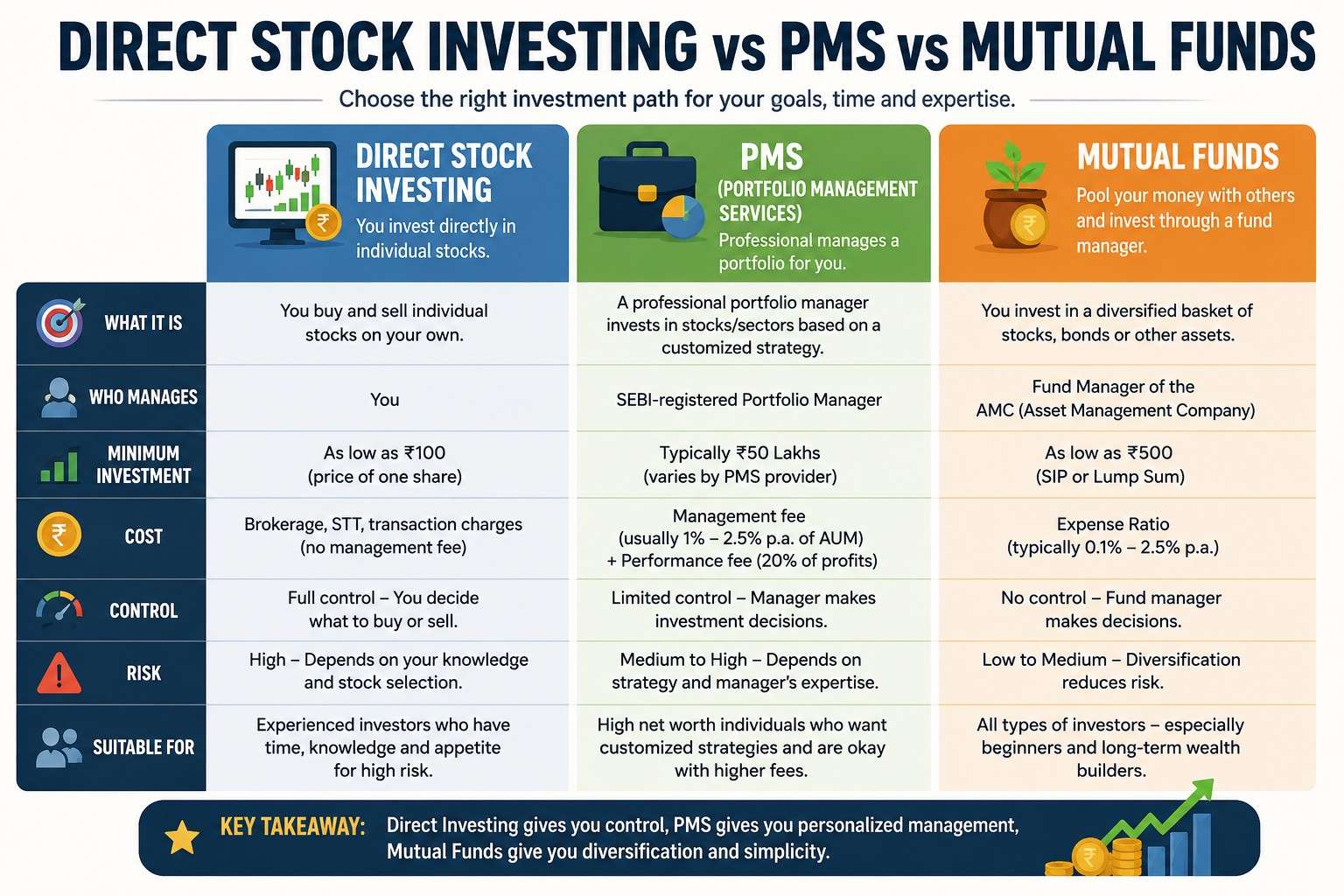

Asset Allocation Basics: How to Build a Balanced Investment Portfolio

-

- June 26th, 2026

- 244 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

Asset allocation basics matter because they determine the long-term balance between risk and return in any investment portfolio. This guide explains the components of allocation, how to create a balanced portfolio, and practical rules for choosing percentages, rebalancing, and measuring outcomes.

- Asset allocation is the split among stocks, bonds, cash, and other asset classes to match risk tolerance and goals.

- Start with a written target allocation, a rebalancing rule, and low-cost funds or ETFs to implement it.

- Use the STEP checklist (Survey, Target, Execute, Periodic review) to build and maintain allocations.

Asset allocation basics: what it is and why it matters

Asset allocation basics cover the decisions about how much of a portfolio goes to equities, fixed income, cash, and alternatives. The split drives both expected returns and volatility; shifting 10% from bonds to stocks can materially change long-term growth and short-term swings. Modern Portfolio Theory (Markowitz) and guidance from organizations such as the CFA Institute establish allocation as a core driver of portfolio outcomes.

How to build a balanced portfolio

Constructing a balanced portfolio follows a repeatable sequence: define objectives, choose an allocation consistent with risk tolerance, and pick investment vehicles that deliver broad exposure at low cost.

Step 1 — Define goals and time horizon

Clarify the purpose of the portfolio (retirement, emergency fund, house down payment) and the time horizon. Short goals (0–5 years) favor liquidity and capital preservation; long goals (10+ years) can tolerate higher equity exposure.

Step 2 — Assess risk tolerance and capacity

Distinguish emotional tolerance (how much loss can be endured) from financial capacity (ability to recover losses). Use simple measures — percent drop that would cause selling — and adjust allocations accordingly.

Step 3 — Choose an allocation and instruments

Common starting allocations: 60/40 (stocks/bonds) for balanced growth, 80/20 for growth tilt, 40/60 for conservative aims. Implement with diversified ETFs or mutual funds across domestic and international equities, core bond funds, and a small cash buffer.

Framework: the STEP checklist

Named framework for practical use:

- S — Survey goals, liquidity needs, and constraints

- T — Target allocation: set percent ranges for major asset classes

- E — Execute with low-cost index funds or diversified securities

- P — Periodic review and rebalancing schedule

Practical tips for portfolio implementation

Actionable points for maintaining a balanced allocation:

- Automate contributions into target allocations using dollar-cost averaging to reduce timing risk.

- Use a rebalancing rule: calendar-based (semiannual) or threshold-based (rebalance when allocation drifts by 5%).

- Prefer broad index funds or ETFs for core exposure to minimize fees and tracking error.

- Document the plan in writing: target percentages, acceptable drift, and tax-aware rebalancing rules.

Short real-world example

Example scenario: A 40-year-old with a 25-year retirement horizon chooses a target allocation of 70% equities / 25% bonds / 5% cash. Equity exposure is split 60% domestic and 40% international. Contributions are automatic each month, and the plan is to rebalance annually or if any asset class deviates more than 6% from the target. Over a five-year market cycle this approach produced expected growth while limiting short-term selling caused by market volatility.

Common mistakes and trade-offs

Key trade-offs and typical errors to avoid:

- Overconcentration: Holding single-stock bets or sector-heavy funds increases idiosyncratic risk.

- Too frequent rebalancing: Excess trading can erode returns through costs and taxes; adopt a sensible schedule.

- Chasing returns: Switching allocations after big recent gains often locks in poor timing and raises costs.

- Ignoring correlation: Assets that appear different may move together in stress; diversify across low-correlation exposures when possible.

Trade-offs

Higher equity weight generally raises expected returns but increases volatility and sequence-of-returns risk. More bonds reduce drawdowns but also lower long-term gains and introduce interest-rate sensitivity. Liquidity needs, tax status, and investment horizon determine the optimal balance.

Measuring success and the role of rebalancing

Success metrics include staying within target risk bands, meeting return expectations relative to liability or goal benchmarks, and avoiding emotional changes to allocation after market moves. For guidance on rebalancing frequency and best practices, many investors reference research and guidance from established firms. See a practical overview of asset allocation and rebalancing strategies here: Vanguard: Asset allocation basics.

Practical portfolio maintenance checklist

Quick maintenance checklist to review quarterly or annually:

- Confirm goals and horizon are unchanged.

- Compare current allocation to target; rebalance if drift exceeds thresholds.

- Check fees and overlap in holdings (avoid duplicate sector or fund exposure).

- Adjust for major life events: job change, inheritance, or large expenses.

FAQ — What is asset allocation basics and why is it important?

Asset allocation basics determine how investment dollars are distributed across asset classes. It’s important because allocation explains most of the variance in long-term portfolio returns and risk profiles, making it the primary decision for aligning investments with financial goals.

How often should a portfolio be rebalanced?

Rebalancing can be calendar-based (annual or semiannual) or threshold-based (rebalance when an asset class drifts by 5–10%). Threshold rules tend to reduce unnecessary trades while calendar rules are easier to automate. Tax implications should guide whether rebalancing occurs inside taxable accounts or retirement accounts.

What is a simple allocation for a conservative investor?

Conservative allocations often range from 30–50% equities and 50–70% bonds and cash. The exact split depends on expected income needs and the investor’s ability to tolerate short-term losses.

How does diversification reduce risk?

Diversification reduces idiosyncratic risk by combining assets whose returns are not perfectly correlated. Proper diversification can lower volatility without proportionally reducing expected returns when low-correlation assets are included.

Can asset allocation be automated?

Yes. Many platforms support automatic contributions into target allocations and automatic rebalancing. Robo-advisors and brokerage account settings offer rules-based rebalancing that follow the STEP checklist and enforce the chosen target allocation.