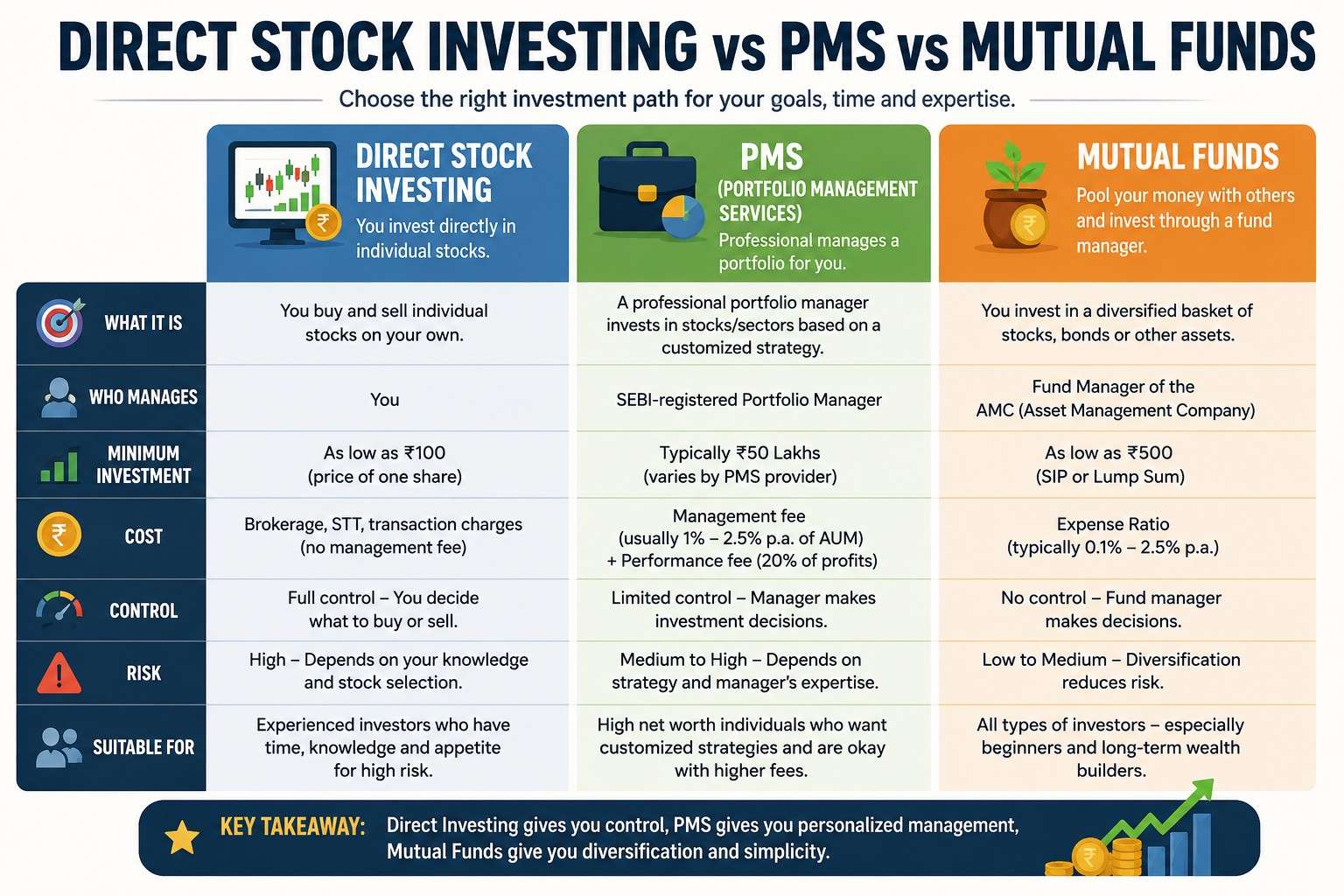

Essential Bond Investing Basics: Fixed-Income Strategies for Stability and Income

-

- June 26th, 2026

- 198 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

Bond Investing Basics: Key Concepts for Fixed Income and Stability

Understanding bond investing basics is essential for investors seeking predictable income and lower portfolio volatility. Bonds are loans to governments, municipalities, or corporations that pay coupon interest and return principal at maturity, and they play a distinct role from stocks in asset allocation, risk management, and cash-flow planning.

- What bonds are: fixed-income securities that pay periodic interest and return principal at maturity.

- Key risks: interest-rate risk (duration), credit/default risk, reinvestment risk, and inflation risk.

- Practical tools: bond ladders, duration targeting, and credit diversification.

- Next steps: match bond choices to purpose (income, preservation, diversification).

bond investing basics: How bonds work and why they provide stability

Core mechanics: a bond’s coupon rate, yield to maturity (YTM), price, and credit rating determine expected return and risk. Bond prices move inversely to interest rates: when rates rise, existing bond prices fall. Duration measures sensitivity of a bond’s price to interest-rate changes and is central to managing interest-rate risk.

Types of bonds and where they fit in a portfolio

Government bonds

Includes sovereign debt such as U.S. Treasury securities. Typically lowest credit risk and high liquidity. Useful for capital preservation and benchmark yields.

Municipal and taxable bonds

Municipal bonds often offer tax-exempt interest at the federal (and sometimes state) level and suit taxable accounts. Compare after-tax yields when evaluating these instruments.

Corporate bonds and high-yield bonds

Corporates provide higher yields but carry greater credit/default risk. Investment-grade vs. high-yield (junk) bonds represent a trade-off between income and credit risk.

fixed income investing strategies: Laddering, barbell, and bullet

Three common approaches to using bonds in a portfolio:

- Bond laddering strategy: Stagger maturities to create predictable cash flows and reduce reinvestment timing risk.

- Barbell: Combine short- and long-term maturities to balance liquidity and yield.

- Bullet: Concentrate maturities at a target date to fund a future liability.

Named framework: BOND Ladder Checklist

Use the BOND Ladder Checklist when building a ladder:

- B — Balance maturities across time horizons (short, medium, long).

- O — Optimize credit quality by mixing issuers and ratings.

- N — Note yield and duration for each rung to control interest-rate sensitivity.

- D — Diversify between taxable and tax-exempt where appropriate.

Duration, yield, and credit: Managing the main trade-offs

Duration measures how much a bond's price is likely to change when interest rates move. A longer duration typically means higher price volatility but often higher yield. Credit ratings from agencies such as S&P Global and Moody’s indicate default risk; conservative portfolios emphasize higher ratings, while income-seeking investors may accept lower ratings for higher yields.

Common mistakes and trade-offs

- Chasing yield: Selecting lower-quality bonds for yield can raise default risk substantially.

- Ignoring duration: Failing to match duration to risk tolerance can create unwanted volatility when rates rise.

- Overconcentration: Holding many bonds from a single issuer or sector increases idiosyncratic risk.

Practical tips for individual investors

- Define purpose: Match bond choices to clear goals (income, capital preservation, or liability matching).

- Use laddering: Implement a bond ladder to smooth reinvestment and provide predictable cash flow.

- Monitor duration: Keep portfolio duration aligned with interest-rate outlook and risk tolerance.

- Check credit diversification: Spread exposure across issuers and sectors to reduce default concentration risk.

- Consider tax impact: Compare taxable vs. tax-exempt yields, especially for high-income taxpayers.

Short real-world example

An investor with a $100,000 fixed-income allocation builds a five-rung bond ladder with maturities at 1, 3, 5, 7, and 10 years. Each rung holds $20,000 split across high-quality corporates and Treasuries. Over time, maturing rungs are reinvested at current rates, smoothing returns and giving consistent cash flow while maintaining diversified credit exposure.

How to evaluate bond prices and funds

Individual bonds hold principal repayment at maturity; bond funds and ETFs provide diversification and professional management but do not return principal at a set date, exposing investors to market-price risk even at a fund’s target maturity equivalent. Compare net expense ratios, duration, and holdings transparency before selecting a fund or ETF.

For official guidance on bond basics and investor protections, see the U.S. Securities and Exchange Commission’s investor education on bonds: SEC: Bonds.

Common considerations: taxes, liquidity, and account placement

Keep liquidity needs in mind: short-term bonds and cash equivalents offer access but low yield. Place tax-advantaged or tax-exempt bonds in taxable accounts as appropriate to maximize after-tax returns, and consider municipal bonds for investors in higher tax brackets.

Practical tips (3–5 quick actions)

- Rebalance periodically to maintain desired duration and allocation.

- Use the BOND Ladder Checklist when building or adjusting a ladder.

- Compare after-tax yields between municipal and taxable bonds for true return.

- Check issuer credit reports and monitor ratings from recognized agencies.

When to use bonds vs. other assets

Bonds suit investors prioritizing income, lower volatility, or liability matching. Stocks are typically better for long-term growth. A balanced portfolio combines equities and fixed income to manage risk across market cycles.

FAQ: What are the essential bond investing basics to know?

Key items: bond definition, coupon vs. yield, duration and interest-rate sensitivity, credit risk, and how chosen bond strategies (laddering, barbell) serve specific financial goals.

How does duration affect bond returns?

Duration estimates price change for a 1% interest-rate move. Use it to size exposure: lower duration reduces volatility when rates rise; higher duration increases sensitivity and potential price gains when rates fall.

Can bonds protect against stock market declines?

Bonds, especially high-quality government bonds, often act as a diversifier and can appreciate when equities fall, but protection is not guaranteed—rising inflation or rates can still hurt bond prices.

What is the difference between bond funds and individual bonds?

Individual bonds return principal at maturity if the issuer does not default. Bond funds provide diversification and liquidity but have no fixed maturity for principal return and are exposed to market-price fluctuations.

How do taxes affect bond returns?

Interest from taxable bonds is subject to income tax; municipal bonds may be tax-exempt at the federal level and sometimes state level. Calculate after-tax yields when comparing options.