Direct Stock Investing vs PMS vs Mutual Funds: Where Does the Line Actually Sit for a ₹25–50 Lakh Portfolio?

-

- August 04th, 2026

- 484 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

Somewhere between ₹25 lakh and ₹50 lakh, most Indian investors hit an uncomfortable question: is it time to move beyond mutual funds? The SIPs have compounded well, the portfolio finally looks substantial on paper, and suddenly PMS brochures, stock tips from relatives, and "graduate to direct equity" advice start arriving from every direction. At Techolic, this is one of the most common conversations we have with clients who've crossed this threshold — and honestly, most of them are asking the wrong question. The right question isn't "which is better," it's "which structure fits my time, temperament, and the actual size of my money."

This article breaks down exactly where direct stock investing, PMS, and mutual funds each make sense for a ₹25–50 lakh portfolio, and where the real line sits.

Where Does the ₹25–50 Lakh Investor Actually Stand Today?

This portfolio band sits in a strange middle zone. It's too large to be casual about, but for most people, still too small to unlock the genuine benefits of a Portfolio Management Service. It's also large enough that the "just keep doing SIPs" advice starts to feel incomplete, even if it's still statistically the right call for most people.

Here's the practical reality: PMS in India requires a minimum investment of ₹50 lakh per SEBI regulations. So if you're sitting at ₹25–30 lakh, PMS isn't even on the table yet — regardless of what a relationship manager promises you. That single regulatory fact quietly resolves half the confusion before we even get to strategy.

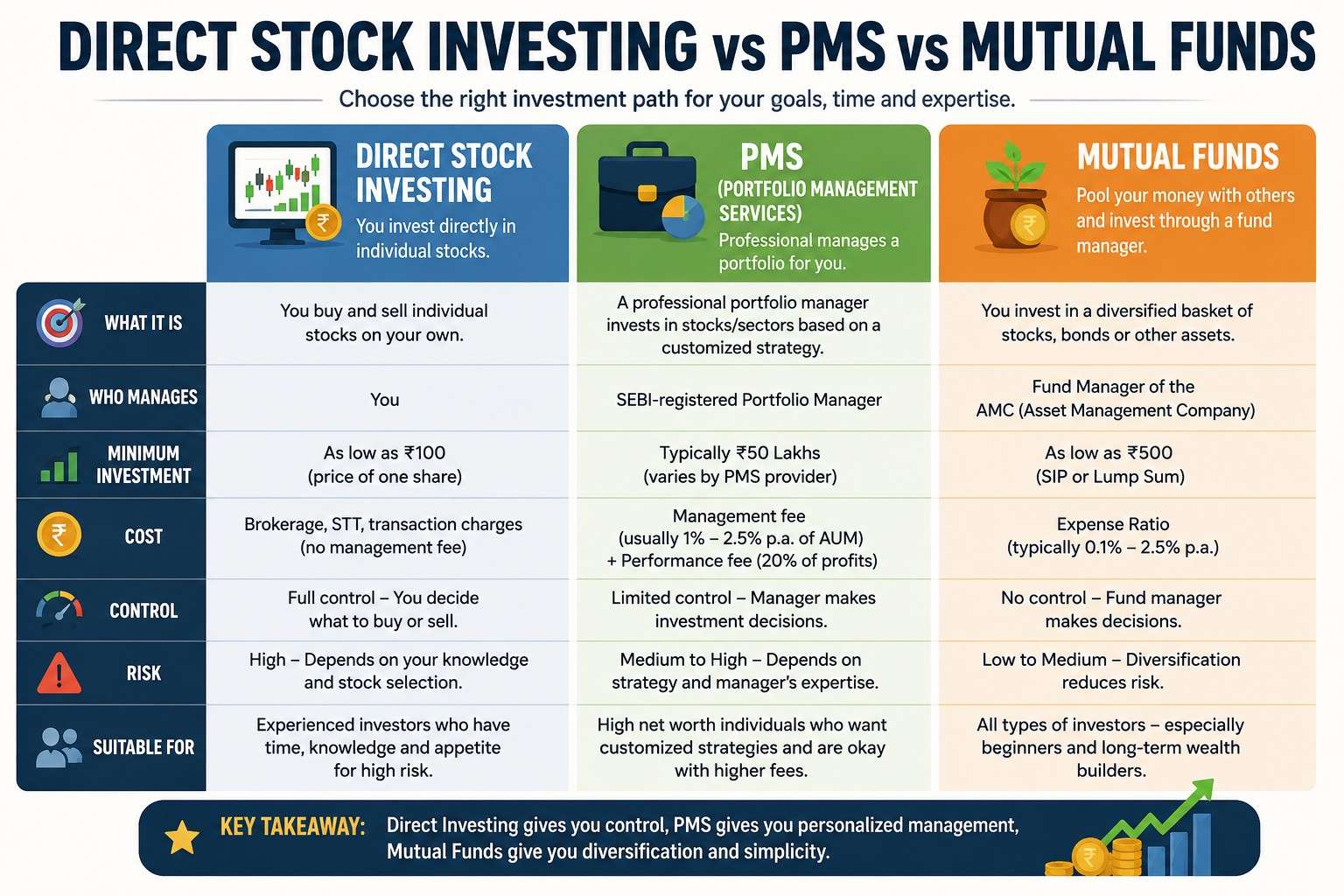

What Is Direct Stock Investing, and Who Is It Really For?

Direct stock investing means buying individual company shares yourself — through Zerodha, Groww, or any broker of your choice — and building your own portfolio stock by stock. No fund manager, no advisory layer, just your own research and decisions.

Direct stock investing genuinely works when:

- You have the time to track quarterly results, management commentary, and sector developments — not occasionally, but consistently

- You understand basic valuation metrics like P/E, P/B, ROE, and debt-to-equity, and can apply them without just copying what's trending on social media

- You're emotionally equipped to hold through a 30–40% drawdown in an individual stock without panic-selling

- You want concentration — the ability to bet meaningfully on 10–15 companies rather than diversifying across hundreds

Where direct stock investing usually goes wrong at this portfolio size is the illusion of diversification. An investor with ₹30 lakh often ends up holding 25–30 stocks picked from broker recommendations, YouTube videos, and WhatsApp forwards, with no coherent strategy tying them together. That's not investing — that's a scattered collection of bets, and it typically underperforms a well-managed mutual fund over a full market cycle.

How Does a Portfolio Management Service (PMS) Work?

A PMS is a professionally managed, concentrated equity portfolio built specifically for one investor, held directly in their own demat account rather than pooled like a mutual fund. A fund manager makes the actual buy and sell decisions on your behalf, based on a defined strategy — value, growth, contrarian, or thematic.

The appeal is straightforward: professional stock-picking without doing the research yourself, combined with the transparency of seeing exactly which stocks you own, since the shares sit in your own demat account and not in a pooled structure.

But PMS comes with real trade-offs that aren't always highlighted upfront:

- The ₹50 lakh minimum investment means it isn't accessible below that threshold, and putting your entire ₹50 lakh into a single PMS strategy concentrates risk in one manager's judgment

- Fees are meaningfully higher than mutual funds — typically a fixed fee of 1.5–2.5% annually, sometimes combined with a performance fee of 10–20% above a hurdle rate

- Returns are not pooled or averaged like a mutual fund NAV — your portfolio's actual holdings and timing of entry can meaningfully differ from another investor in the same PMS strategy

- Exit isn't always smooth; unwinding a concentrated PMS portfolio can trigger capital gains at less convenient times than a mutual fund redemption would

For a ₹50 lakh portfolio, putting the entire amount into one PMS strategy is rarely the right call. It works better as one component of a larger allocation, not the whole portfolio.

Where Do Mutual Funds Fit Into a ₹25–50 Lakh Portfolio?

Mutual funds remain the backbone for most investors in this bracket, and there's a good reason for that beyond habit. A mutual fund gives you professional management, built-in diversification across dozens of stocks, daily liquidity, and a cost structure that's transparent and regulated under the newly restructured Total Expense Ratio norms.

At ₹25–50 lakh, mutual funds work particularly well because:

- You can diversify across market caps, sectors, and even fund managers without needing ₹50 lakh per strategy the way PMS demands

- SIP and STP structures let you deploy money gradually, reducing timing risk in a way that a lump-sum PMS or direct stock purchase doesn't naturally offer

- The lower ticket size per fund means you can build a genuinely diversified core — a large-cap fund, a flexi-cap fund, maybe a small allocation to a focused fund — without over-concentrating in any single strategy

The common mistake here is over-diversification in the opposite direction — investors holding eight or nine mutual funds that essentially overlap in their underlying stocks, paying for diversification they never actually get. Three to five well-chosen funds usually cover this portfolio size more efficiently than eight or ten.

Direct Stocks vs PMS vs Mutual Funds — Where Does the Line Actually Sit?

Here's how we'd frame the decision at Techolic when a client's portfolio crosses into this range:

Under ₹35 lakh, mostly mutual funds. This is the size where diversification and professional management matter more than customization. A core of 3–4 mutual funds, split across large-cap, flexi-cap, and possibly a mid-cap allocation depending on risk appetite, does the heavy lifting.

₹35–50 lakh, mutual funds with a small direct equity satellite. If you genuinely enjoy tracking markets and have the time, carve out 10–15% of the portfolio for direct stocks in companies you understand deeply — not as a replacement for your core, but as a satellite that lets you engage without risking the whole portfolio on your own stock-picking skill.

At ₹50 lakh and above, PMS becomes a genuine option — but only as a slice, not the whole pie. Even once the ₹50 lakh minimum is met, allocating your entire liquid net worth to one PMS strategy concentrates both manager risk and stock-specific risk. A more balanced structure keeps 50–60% in mutual funds for stability and liquidity, and allocates the rest to PMS or direct equity based on genuine interest and risk tolerance.

The line isn't really about which product is "better" — it's about matching the structure to how much time you have, how much concentration risk you can stomach, and how the fee structure affects your net returns over a 10-year horizon rather than a single year.

What Are the Common Mistakes Investors Make at This Portfolio Size?

- Chasing PMS purely for prestige. Many investors move to PMS the moment they cross ₹50 lakh simply because it feels like a status upgrade, without evaluating whether the manager's strategy, fee structure, and track record actually justify the cost over their existing mutual fund returns

- Treating direct stocks as a hobby with real money. Tracking stocks casually on weekends isn't the same discipline required to manage a serious equity allocation — and the gap between the two shows up in returns

- Ignoring tax implications of switching structures. Moving from mutual funds to PMS, or liquidating direct stock holdings to fund a PMS minimum, can trigger LTCG or STCG that eats into the very gains you're trying to preserve

- Comparing PMS returns to mutual fund NAVs directly. PMS returns are often quoted pre-fee or based on a model portfolio, not your actual account performance — always ask for your own portfolio's post-fee, post-tax returns before comparing

- Underestimating how much time direct equity actually demands. Even a modest 15% satellite allocation in direct stocks needs quarterly attention; treating it as "set and forget" defeats the purpose of holding individual stocks at all

So Where Should Your ₹25–50 Lakh Actually Go?

There's no universal answer, and anyone who gives you one without understanding your income stability, risk appetite, and time availability isn't giving you advice — they're giving you a product pitch. What we've seen work consistently at Techolic (https://techolic.co.in/) is starting with a strong mutual fund core, adding direct equity only if there's genuine interest and bandwidth, and treating PMS as something to graduate into gradually rather than jump into the moment the minimum ticket size is met.

The size of your portfolio tells you what's possible. It doesn't tell you what's right for you — that still depends on how much time, temperament, and attention you're willing to bring to the table.

Frequently Asked Questions

Is ₹50 lakh really the minimum for PMS in India?

Yes, SEBI mandates a minimum investment of ₹50 lakh for Portfolio Management Services. This applies uniformly across PMS providers and cannot be waived, regardless of the strategy or fund house.

Can I combine PMS, mutual funds, and direct stocks in one portfolio?

Absolutely, and for portfolios above ₹50 lakh, this combination is often the most balanced approach — mutual funds for the diversified core, PMS for concentrated professional exposure, and direct stocks for companies you understand well enough to hold with conviction.

Is direct stock investing riskier than mutual funds?

It depends entirely on execution. A well-researched, disciplined direct stock portfolio isn't inherently riskier than mutual funds, but a scattered collection of stocks bought without a clear strategy usually underperforms and carries higher volatility than a diversified mutual fund.

Do PMS returns beat mutual fund returns?

Not consistently. Some PMS strategies outperform in certain market cycles, especially in concentrated bull runs, but they can also underperform sharply during corrections due to lower diversification. Post-fee, post-tax comparison over a full market cycle is the only fair way to judge this.

At what portfolio size should I stop relying only on mutual funds?

There's no fixed number, but most investors start considering a direct equity satellite once their portfolio crosses ₹30–35 lakh and they have both the time and inclination to track individual stocks actively.

How much of my portfolio should go into direct stocks if I'm just starting out with them?

A commonly used starting point is 10–15% of your total equity allocation, kept as a satellite around your mutual fund core, so early mistakes don't derail your overall financial goals.