Practical Dividend Calculator Guide for Stock and Mutual Fund Income Planning

-

- March 30th, 2026

- 245 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

A dividend calculator helps estimate the portfolio size needed to produce a specific annual income from dividends and distributions. Use a dividend calculator to compare stocks and mutual funds, account for taxes and withdrawal schedules, and test scenarios like reinvestment, yield changes, and inflation.

- Enter the target annual income, expected yield, tax rate, and payout frequency to estimate required principal.

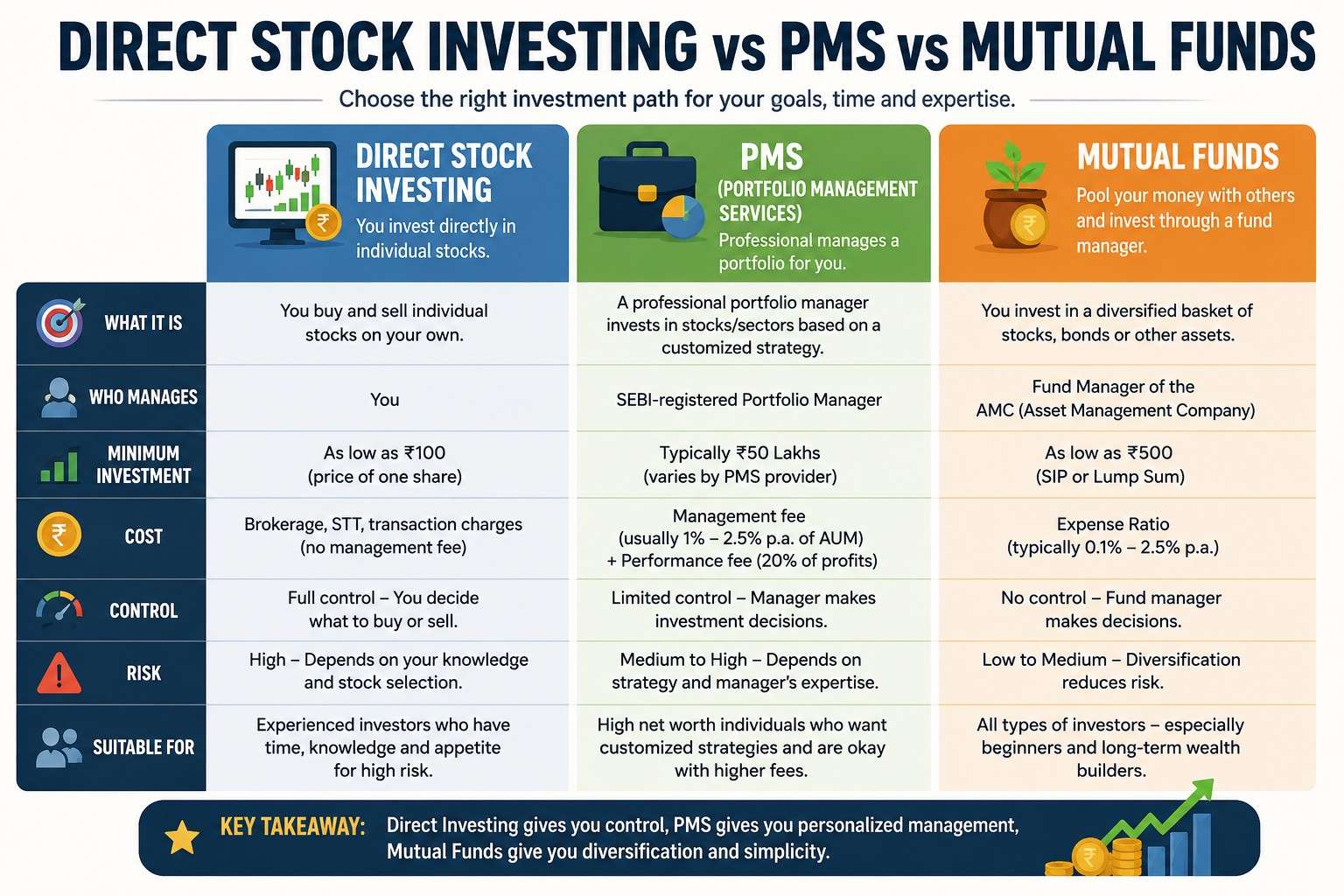

- Compare stock dividend calculators with mutual fund distributions—fund yields often include capital gains and fees.

- Use the DIVIDE model checklist to validate assumptions and include safety margins for volatility and taxes.

How to use a dividend calculator for income planning

Start with a clear target income, then input realistic yield rates and tax assumptions into the dividend calculator. The basic formula used by most tools is: Required Principal = Target Annual Income / Net Yield, where Net Yield = Gross Yield × (1 − Tax Rate) − Fees/Expenses.

Step-by-step calculator workflow

- Set the target annual cash income needed (for example, $20,000).

- Choose an expected gross yield (a stock dividend yield or a mutual fund distribution yield).

- Add expected taxes and recurring fees to get a net yield assumption.

- Calculate principal and test sensitivity: what if yield falls 0.5% or tax rate rises 5%?

- Decide payout schedule (monthly, quarterly) and plan cash-flow timing.

DIVIDE model: a checklist for reliable planning

Use the DIVIDE model as a named framework to validate a dividend income plan:

- Define goal: exact annual income and time horizon.

- Input yields: current dividend or distribution yields for chosen assets.

- Verify taxes/fees: expected tax rate, fund expense ratios, and broker fees.

- Include volatility: stress-test yield drops and price declines.

- Distribution schedule: match payout timing to cash needs.

- Estimate growth: project dividend growth or cuts over time.

Key inputs for a stock dividend calculator and mutual fund comparisons

Essential input fields

- Target annual income (cash required each year).

- Gross dividend or distribution yield (annual percentage).

- Expected tax rate on dividends/distributions (qualified vs ordinary).

- Expense ratios or management fees for mutual funds.

- Assumptions about future yield growth or cuts and reinvestment.

Mutual funds and ETFs list distribution yields that can include return of capital, capital gains, and interest—so mutual fund income planning must separate recurring income from one-time gains. For federal guidance on dividend and distribution reporting practices, consult the Securities and Exchange Commission: SEC investor bulletin on dividends.

Real-world example: calculating required capital

Scenario: A target of $20,000 per year in dividend income. Two cases:

- Using an average stock dividend yield of 3.0% (gross) and a 15% effective tax on qualified dividends: Net Yield = 0.03 × (1 − 0.15) = 0.0255 (2.55%). Required Principal = 20,000 / 0.0255 ≈ $784,314.

- Using a mutual fund distribution yield of 1.8% with a 0.5% expense ratio and 15% tax: Net Yield ≈ (0.018 − 0.005) × (1 − 0.15) = 0.01105 (1.105%). Required Principal = 20,000 / 0.01105 ≈ $1,810,861.

These calculations show how yield and fees dramatically change required capital. A dividend yield calculator should let users toggle taxes and fees to see these effects.

Practical tips for more accurate results

- Use conservative yield estimates—use a lower bound (e.g., 10–20% below current yield) to stress-test plans.

- Include taxes, expense ratios, and broker fees as separate inputs rather than implicit adjustments.

- Run sensitivity analysis: test required capital at several yield scenarios (best, base, worst).

- Factor in inflation and a withdrawal safety buffer (a common rule is adding 10–25% extra principal for market risk).

Common mistakes and trade-offs

- Assuming current yield is permanent: dividends can be cut; funds can change distributions.

- Ignoring fees and taxes: small percentage points erode income over time.

- Chasing high yields without credit quality checks: very high yields often indicate elevated risk.

- Over-relying on yield instead of total return: dividends are only one component of investor returns.

When to prefer stocks vs mutual funds for income

Stocks can offer higher yields and potential dividend growth but require individual security selection and monitoring. Mutual funds or ETFs simplify diversification and automatic cash distributions but include management fees and sometimes lower yields. The trade-off is control and yield versus diversification and convenience.

Practical implementation checklist

- Run the dividend yield calculator with gross and net yield inputs.

- Apply the DIVIDE model checklist to validate assumptions.

- Save scenarios and re-run annually or when market yields shift.

FAQ

How does a dividend calculator estimate required principal?

It divides the target annual income by an estimated net yield (gross yield adjusted for taxes and fees) to compute the principal needed to produce that income.

Can a stock dividend calculator account for dividend growth?

Yes—include a projected dividend growth rate or run multi-year scenarios to reflect compounding and yield changes over time.

Is a mutual fund income planning approach different from stocks?

Mutual fund income planning must include expense ratios, distribution composition (income vs capital gains), and potential return-of-capital items, which affect sustainable income differently than stock dividends.

What common errors should be avoided when using a dividend calculator?

Avoid assuming current yields are guaranteed, ignoring taxes and fees, and selecting assets based solely on the highest yield without assessing sustainability and diversification.

Where can official guidance on dividend reporting be found?

Refer to the Securities and Exchange Commission investor resources for authoritative guidance on dividends and distributions: see the SEC investor bulletin linked above.