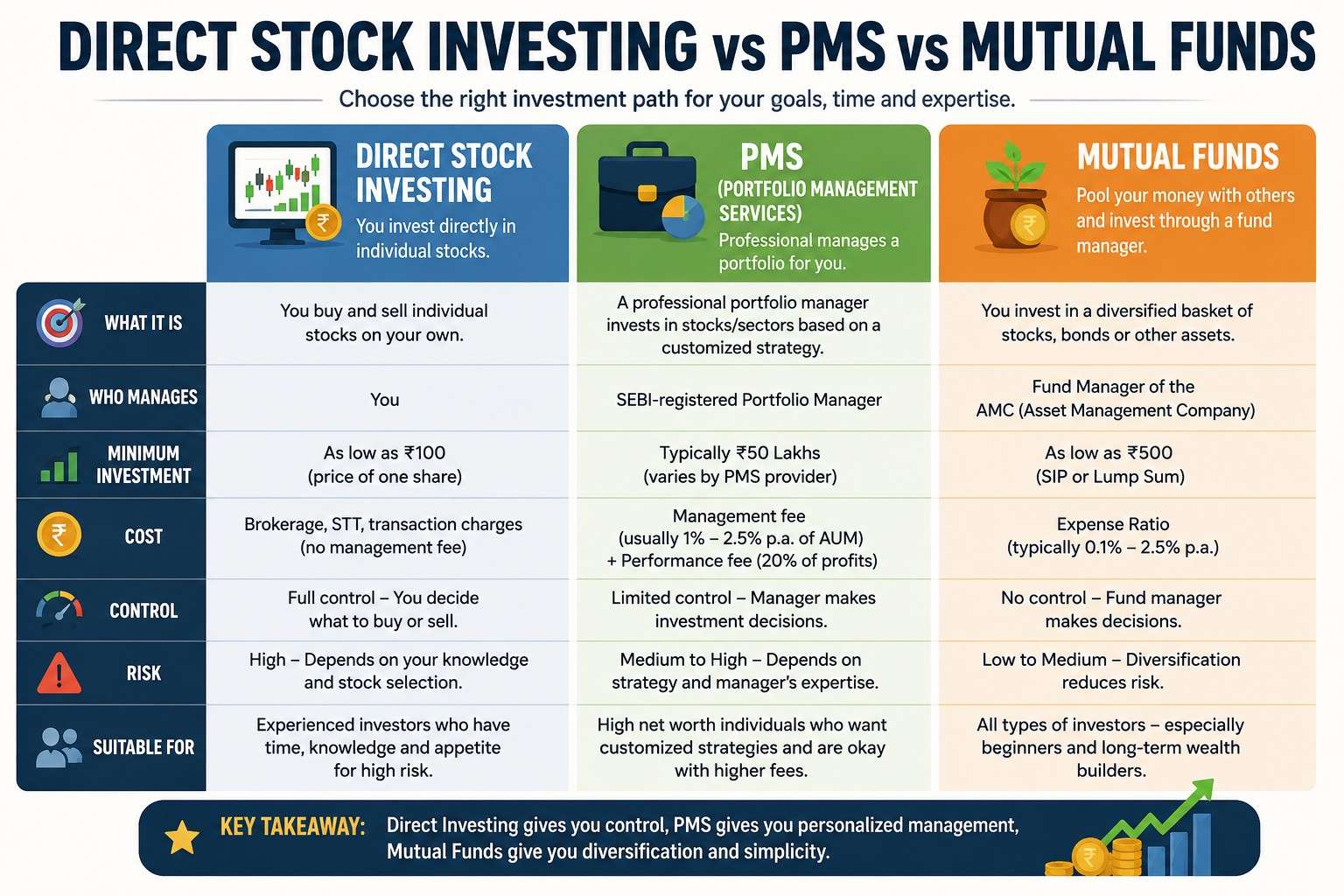

Domestic vs International Investing: A Practical Global Investing Overview

-

- June 26th, 2026

- 268 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

Comparing domestic vs international investing requires evaluating differences in risk drivers, return opportunities, costs, and portfolio role. Domestic vs international investing decisions affect diversification, currency exposure, and how political or economic events influence portfolio returns.

- Domestic investing favors familiarity, lower currency and tax friction, and access to local sectors.

- International investing offers diversification, exposure to faster-growing economies, and unique sector weights, but adds currency, regulatory, and emerging-market risks.

- Use a simple checklist (GLOBE) to decide allocation, and follow practical tips: define goals, measure home-country bias, use low-cost vehicles, and rebalance.

Domestic vs International Investing: Key differences and why they matter

Domestic investments typically include local-listed stocks, bonds, and funds. International investments span developed and emerging markets, foreign-listed securities, American Depositary Receipts (ADRs), and cross-listed ETFs. The primary differences come from currency exposure, geopolitical risk, sector composition, and correlation patterns. These factors determine whether international market investing strategies will improve risk-adjusted returns or simply add complexity.

How international exposure changes portfolio behavior

Returns and growth opportunities

Many markets outside a home country may have faster nominal GDP growth or different sector concentrations (for example, higher commodity exposure in some emerging markets). That can translate into higher potential returns, but performance varies by country and cycle.

Risk factors: currency, political, and liquidity risk

Foreign investments add currency risk (FX moves can boost or reduce local returns), political/regulatory risk, and in some markets, lower liquidity. These are common considerations in international market investing strategies.

Diversification and correlation benefits

Adding international assets often reduces overall portfolio correlation during long-term periods, which supports global portfolio diversification. For a formal view on diversification as a risk-management practice, official investor guidance explains the benefits and limits of diversification: U.S. Securities and Exchange Commission — Diversification.

The GLOBE checklist: a named framework for allocation decisions

Apply the GLOBE checklist before changing international exposure. GLOBE is a compact decision framework:

- Goals — Match global exposure to time horizon and return needs.

- Liquidity — Ensure access to cash and account for settlement differences.

- Oversight — Understand tax, reporting, and custodian implications.

- Bias check — Measure home-country bias and consciously decide on it.

- Exposure — Select vehicles and hedge options for currency and sector exposure.

Practical example: reallocating from domestic-heavy to balanced global

Scenario: A conservative investor holds 80% domestic equities and 20% domestic bonds. After measuring correlation and home-country bias, the investor decides to target 60% domestic equities, 20% international equities, and 20% bonds.

Result: The 20% shift to international equities adds exposure to sectors underrepresented domestically (for example, consumer staples in Europe or technology in Asia) and lowers portfolio correlation in many historical periods. The investor limits currency exposure by choosing hedged international bond funds but keeps unhedged international equity ETFs to capture potential currency gains.

Practical tips for implementing international exposure

- Define a clear target allocation and treat international exposure as a strategic allocation, not a market-timing play.

- Use low-cost, tax-efficient vehicles (index funds and ETFs) to access broad regions or factor exposures.

- Decide on currency policy: hedge bonds if income stability is primary; consider unhedged equities for longer horizons.

- Account for tax and reporting differences in brokerage and retirement accounts before buying foreign securities.

- Rebalance periodically to maintain the target international share and avoid drift from home-country bias.

Trade-offs and common mistakes when choosing international exposure

Common mistakes

- Overcomplicating with many single-country positions instead of broad ETFs or funds, increasing tracking and implementation risk.

- Ignoring currency effects—both upside and downside—when evaluating past performance.

- Underestimating tax and withholding implications, especially for dividends from foreign issuers.

Key trade-offs

- Stability vs. growth: Domestic markets may feel safer, while international markets can offer higher growth but higher volatility.

- Simplicity vs. precision: Global funds are simple; country-specific positions provide precision but require research and monitoring.

- Cost vs. control: Hedging currency reduces volatility but increases cost and can reduce long-term returns.

Vehicle choices and practical mechanics

Common instruments

Options include international mutual funds, global or regional ETFs, ADRs for single foreign companies, and direct foreign-listed shares. Bond exposure offers currency-hedged and unhedged funds, and investors can use country or global sovereign bonds for diversification.

Measuring home-country bias

Compare domestic market cap share of a global market-cap index to the investor's domestic equity weight. A large gap signals home-country bias and can guide rebalancing decisions.

FAQ

What is domestic vs international investing and which is better for diversification?

Domestic vs international investing contrasts local securities with assets from other countries. Neither is universally better—international investing often improves diversification and access to growth, while domestic investing reduces currency and certain regulatory risks. The right mix depends on goals, time horizon, and risk tolerance.

How much of a portfolio should be allocated to international equities?

There is no single correct percentage. Common starting points are 20–40% of equities in international markets, adjusted for goals, tax situation, and tolerance for currency and geopolitical risk.

Do international investments always increase risk?

Not always. They add different types of risk (currency, political), but they can reduce overall portfolio volatility through lower correlations and sector diversification when combined with domestic assets.

What are low-cost ways to get international exposure?

Broad international or global ETFs and index mutual funds provide low-cost, diversified exposure across developed and emerging markets, minimizing single-country risk.

How should home-country bias be measured and corrected?

Measure bias by comparing current domestic weight to global market-cap benchmarks. Correct it gradually—use rebalancing and incremental purchases to move toward a chosen strategic allocation.

Further reading

Official investor resources such as the U.S. Securities and Exchange Commission and recognized industry bodies provide guidelines on diversification, tax reporting, and cross-border investment rules.