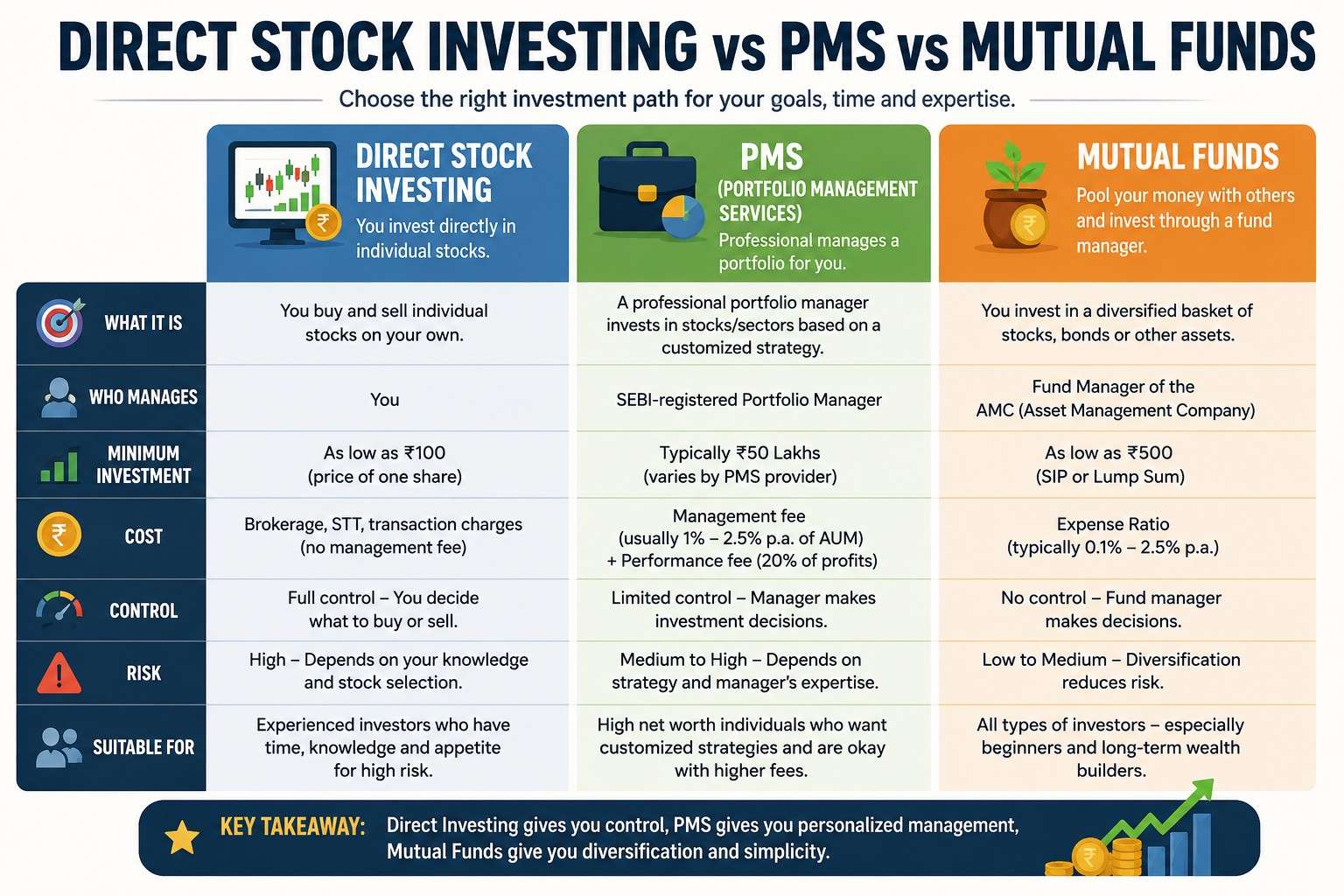

Mutual Funds vs ETFs: Practical Guide to Collective Investment Models

-

- June 25th, 2026

- 269 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

Understanding the differences between mutual funds vs ETFs helps investors choose the collective investment vehicle that matches their goals, tax situation, and trading preferences. This guide explains how each model works, the trade-offs to consider, a practical decision checklist, a short real-world scenario, and actionable tips for everyday investors.

- Mutual funds pool money and are priced once per day using NAV; ETFs trade intraday like stocks.

- Key differences: trading mechanics, liquidity, tax efficiency, and typical fee structures.

- Use the FUND checklist below to evaluate which collective investment vehicle fits a specific goal.

mutual funds vs ETFs: core differences

Mutual funds and exchange-traded funds (ETFs) are collective investment vehicles that combine many investors' capital to buy diversified portfolios of stocks, bonds, or other assets. The primary differences lie in how shares are created and redeemed, when pricing happens, and how investors buy and sell shares. This section breaks down those distinctions with common terms such as NAV (net asset value), expense ratio, load fees, bid-ask spread, creation/redemption mechanism, and passive vs active management.

How each model works

Mutual funds: Shares are issued and redeemed directly with the fund company at the end-of-day NAV. Many mutual funds (including index mutual funds) are designed for buy-and-hold investors and can have front- or back-end loads, redemption fees, or minimum investment amounts.

ETFs: Shares trade on an exchange throughout the day at market prices that can deviate slightly from NAV. Authorized participants create and redeem large blocks of ETF shares via in-kind transfers, which often improves tax efficiency. The intraday liquidity and ability to place limit orders are important for certain strategies.

Costs, taxes, and liquidity

Costs: Expense ratios are the baseline ongoing cost for both products. ETFs often have lower expense ratios for passive strategies, but investors may pay brokerage commissions or incur bid-ask spread costs when trading.

Taxes: The ETF creation/redemption mechanism often reduces capital gains distributions compared with mutual funds, making ETFs generally more tax-efficient for taxable accounts. Tax-sensitive investors should confirm distribution history and structure.

Liquidity: Mutual fund liquidity settles at NAV once per day; ETFs offer intraday liquidity but actual tradability depends on market liquidity and the bid-ask spread.

For official guidance on mutual fund rules and investor protections, see the U.S. Securities and Exchange Commission investor education resources: SEC Investor.gov.

Which model fits different goals — the FUND checklist

Use the FUND checklist to evaluate choices between collective investment vehicles:

- Fees: Compare expense ratios, trading commissions, and potential load fees.

- Underlying strategy: Active vs passive, index tracking accuracy, and turnover.

- NAV and tax impact: Check historical distributions, realized capital gains, and tax efficiency.

- Delivery and liquidity: Trading needs, intraday pricing, and minimum investment requirements.

This named checklist helps compare options consistently across asset classes and account types.

Practical example and scenario

Scenario: A taxable account investor plans to build a diversified equity allocation and prefers low cost and tax efficiency. Using the FUND checklist: Fees — compare expense ratios for similar index mutual funds and ETFs; Underlying strategy — both track the same index; NAV and tax impact — ETFs show lower distributions historically; Delivery and liquidity — ETFs allow intraday rebalancing if needed. For a buy-and-hold target-date allocation, an index mutual fund may be adequate; for periodic taxable rebalancing, an ETF may reduce capital gains.

Practical tips

- Match the product to the account type: ETFs often suit taxable accounts for tax efficiency; mutual funds can be simpler inside tax-advantaged accounts.

- Always compare total costs: include expense ratio, bid-ask spread, and possible commissions.

- Check tax distribution history: funds publish realized capital gains in annual reports and shareholder documents.

- Use limit orders for ETFs to control execution price; use dollar-cost averaging for mutual funds with minimum investments.

Common mistakes and trade-offs

Trade-offs exist between convenience and control. Common mistakes include:

- Choosing a fund based only on headline expense ratio without evaluating tracking error, spread, or tax history.

- Assuming all ETFs are tax-efficient—some actively managed ETFs or those with high turnover can generate taxable events.

- Ignoring transaction costs: frequent ETF trading can erode the advantage of a lower expense ratio.

Deciding between liquidity (intraday trading) and simplicity (automatic investments in mutual funds) requires prioritizing investor behavior and tax consequences.

How to compare index mutual funds and ETFs for the same exposure

Compare these metrics: expense ratio, tracking error to the index, turnover rate, historical distributions, bid-ask spread (for ETFs), minimum investment, and whether automatic investment or dividend reinvestment is available. Include synonyms and related terms in the review, such as passive investing, benchmark tracking, NAV per share, creation/redemption, and bid-ask spread analysis.

FAQ: What is mutual funds vs ETFs and which should be used?

Answer: The choice depends on tax situation, trading needs, and cost sensitivity. Use the FUND checklist above to identify priorities and compare specific fund share classes and ETF trading characteristics.

FAQ: Are ETFs always cheaper than index mutual funds?

Answer: Not always. ETFs often have lower expense ratios for popular passive strategies, but total cost includes trading spreads and commissions. Compare the all-in cost for the intended holding period.

FAQ: How do taxes differ between ETFs and mutual funds?

Answer: ETFs commonly use in-kind creation/redemption to limit capital gains distributions, improving tax efficiency in taxable accounts. Mutual funds with high turnover may distribute realized gains to investors.

FAQ: Can automatic investing be used with ETFs?

Answer: Automatic investing and reinvestment are available for some ETFs through broker services, but mutual funds typically provide simpler built-in automatic investment plans.

FAQ: How to evaluate collective investment vehicles for a retirement portfolio?

Answer: Prioritize expense ratios, tax treatment in account type, and whether the product supports automatic allocations or target-date strategies. For more regulatory details on mutual funds, see the resources provided by established securities regulators and investor education groups.