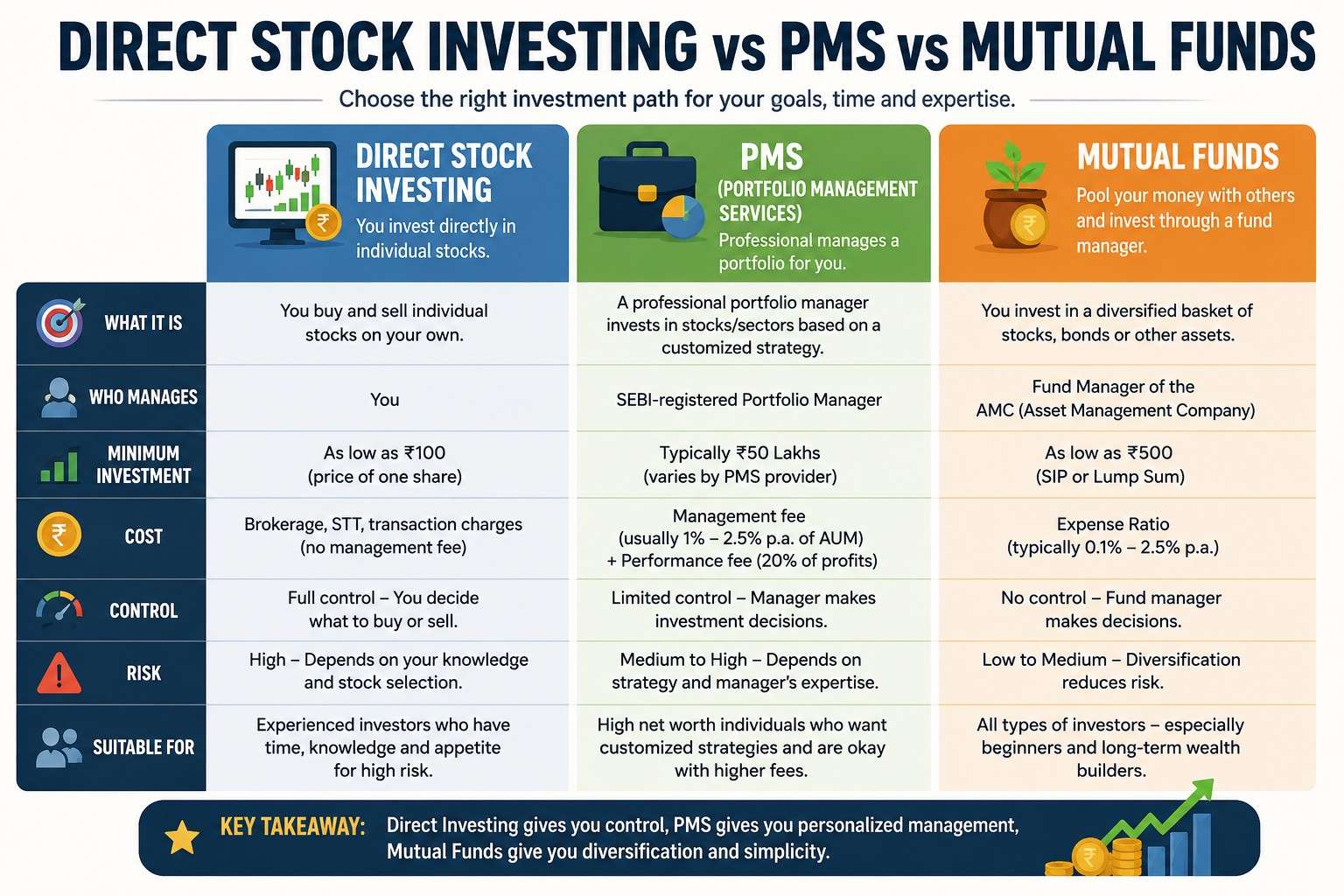

Passive vs Active Investing: How to Choose the Best Strategy for Your Portfolio

-

- June 26th, 2026

- 228 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

Investors often face a core decision: passive vs active investing. That choice affects portfolio costs, tax efficiency, risk exposures, and the likelihood of outperforming market benchmarks. This guide compares both approaches, explains trade-offs, and gives a practical decision checklist to help select the right mix for a portfolio.

Passive vs Active Investing: core definitions and differences

What passive investing means

Passive investing buys a portfolio designed to replicate an index (S&P 500, total market, bond indices). Common vehicles include index mutual funds and ETFs. The main selling points are low expense ratios, low turnover (tax efficiency), and predictable tracking to market returns.

What active investing means

Active investing relies on human or systematic managers making security-selection, sector-tilt, or timing decisions to try to beat a benchmark. Active management strategies vary: concentrated stock-picking, quantitative models, tactical asset allocation, and sector rotation. Active strategies can deliver alpha but also charge higher fees and may underperform benchmarks after costs.

Key metrics to compare

- Expense ratio and total cost of ownership

- Tracking error and active share (how far holdings deviate from the index)

- Historical alpha and consistency vs benchmark

- Turnover rate and tax impact

How to choose: the INVEST checklist

Apply a repeatable framework when deciding between passive and active. The INVEST checklist helps make the trade-offs explicit:

- Identify goals — growth, income, capital preservation.

- Needed timeframe — short-term vs multi-decade horizon.

- Verify costs — fees, spreads, expected tax drag.

- Evaluate risk tolerance and required diversification.

- Select where active skill is plausible (inefficient markets like small caps or certain niches).

- Track performance and re-assess annually.

Where active can make sense

Active management is more likely to add value in less-efficient segments (small-cap equities, emerging markets, certain credit niches) or for investors seeking concentrated bets. However, it's essential to confirm manager skill with long-term, risk-adjusted metrics — not short-term performance alone.

Index fund vs active fund: a short example scenario

Consider two investors over a 10-year horizon. Investor A uses broad market index funds with a combined expense ratio of 0.06% and rebalances annually. Investor B selects an actively managed equity fund charging 0.90% with higher turnover. If the active fund achieves gross outperformance of 1.0% annually, net alpha after fees is ~0.10% — roughly breakeven with risk and tax differences. In many cases, active funds fail to sustain that gross outperformance, so the index approach often wins net of costs. Real-world results vary by market, manager, and time frame.

Costs, taxes, and performance persistence

Costs compound. A 0.5% to 1.0% higher fee reduces compounded returns meaningfully over decades. Turnover increases taxable distributions for taxable accounts. For neutral guidance on fund fees and investor protection, official resources like the SEC offer basic investor education and fund fee explanations: SEC Investor Education.

Common mistakes when choosing passive or active

- Chasing recent active winners without checking long-term consistency.

- Underestimating fee drag and the compounding effect of costs.

- Picking active funds without a plan for measuring skill or exit criteria.

- Ignoring tax consequences of high-turnover strategies in taxable accounts.

Practical tips for implementing either approach

- Match strategy to market segment: prefer passive for broad-cap U.S. equities; consider active for small-cap, niche credit, or inefficient international markets.

- Use low-cost index funds or ETFs for core holdings and reserve a limited sleeve for active bets (e.g., 10–20% of the portfolio).

- Monitor active funds with risk-adjusted metrics (Sharpe ratio, Information Ratio) and require a clear, repeatable edge before allocating meaningful capital.

- Minimize trading frequency and be mindful of tax wrappers (use tax-advantaged accounts for high-turnover active strategies when possible).

- Re-evaluate allocations annually using the INVEST checklist above.

Trade-offs and decision factors

Choosing between passive vs active investing is not binary. The key trade-offs include:

- Cost vs potential alpha: lower fees vs possibility of outperformance.

- Predictability vs manager dependence: reliable benchmark tracking vs reliance on manager skill.

- Tax efficiency vs tactical flexibility: passive funds tend to be tax-friendlier.

Common mistakes recap

Avoid overconcentration in unproven active managers, ignore fees, or assume past performance guarantees future results. Instead, combine low-cost core holdings with targeted active allocations where evidence of skill exists.

FAQ

Is passive vs active investing better for long-term retirement accounts?

For many long-term retirement accounts, passive investing is advantageous due to lower fees and compounding benefits. However, a small allocation to active strategies can be appropriate if the active manager has demonstrated consistent, risk-adjusted outperformance.

How does the index fund vs active fund decision affect taxes?

Index funds typically have lower turnover and therefore fewer taxable distributions in taxable accounts. Active funds with higher turnover may generate short-term gains, increasing tax bills. Use tax-advantaged accounts for higher-turnover strategies.

What indicators show an active manager's skill rather than luck?

Look for multi-year positive alpha, consistent performance across market cycles, high information ratio, low correlation to crowded bets, and a documented, repeatable investment process.

Can a blended approach work and how to size it?

A blended approach (core-satellite) often works well: keep 70–90% in passive core holdings for market exposure and low cost, and 10–30% in active satellites where skill likelihood is higher or diversification benefits are desired.

How should fees and expenses influence the passive vs active investing choice?

Fees are a primary determinant of net returns. Lower expense ratios favor passive strategies unless active management can demonstrably and consistently overcome the fee differential after taxes and costs. Always model net-return scenarios before allocating capital.