India Buy Now Pay Later Market: Segmentation and Competitive Landscape

-

- March 25th, 2026

- 4,288 views

FREE SEO Topical Map Generator: Find Your Next Content Ideas

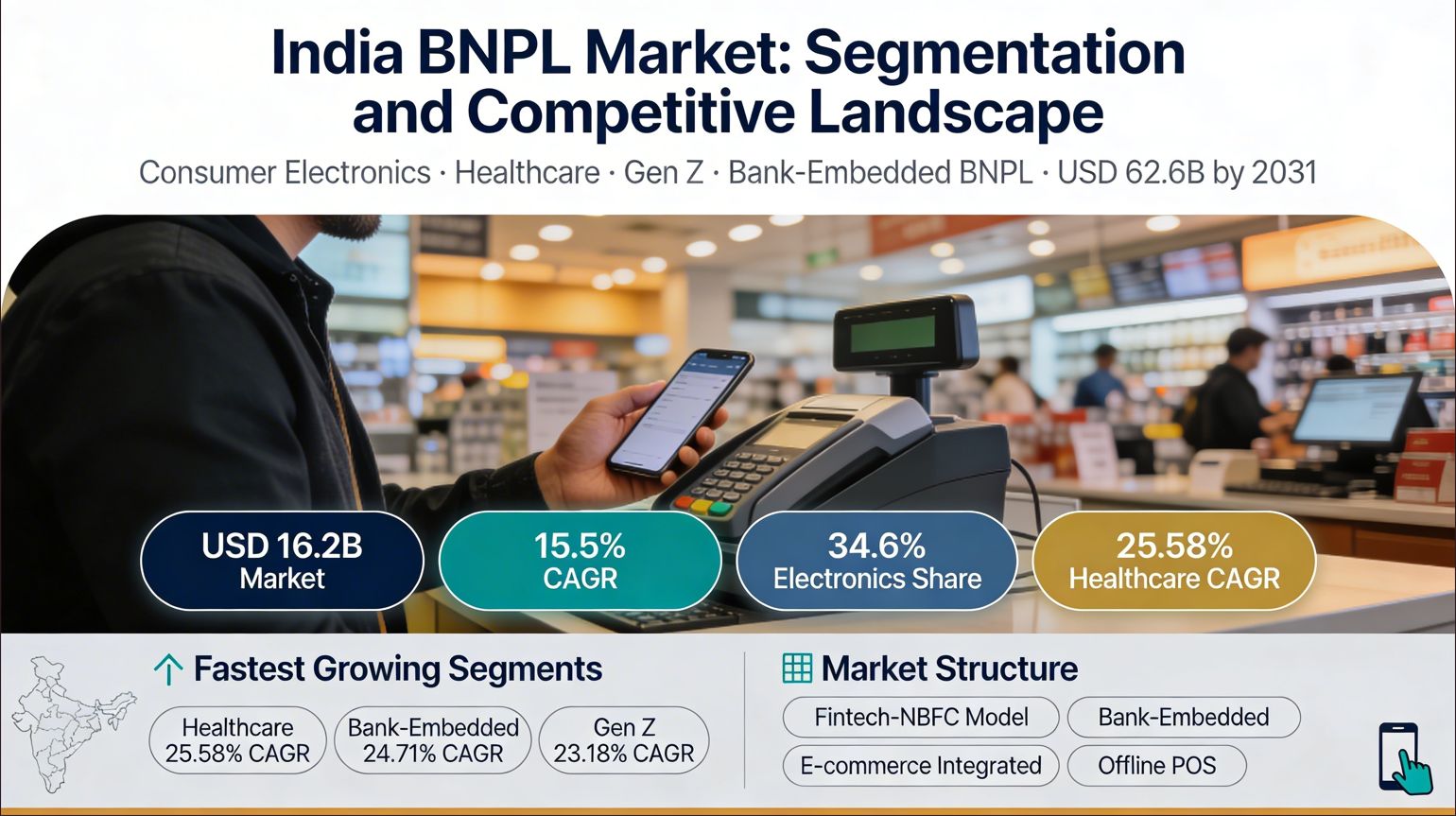

The India Buy Now Pay Later (BNPL) market is valued at approximately USD 16.2 billion in 2024, growing at a CAGR of 15.5% through 2031 to reach an estimated USD 62.6 billion. India is among the fastest-growing BNPL markets globally - where a 500 million+ smartphone user base, a credit-underserved population of over 600 million, and a UPI infrastructure processing 10 billion+ transactions monthly have created conditions for deferred payment adoption at an unmatched scale. The 2022-23 RBI regulatory reset eliminated weaker pure-play fintechs, accelerated bank-fintech partnerships, and produced a more regulated, bank-anchored BNPL ecosystem that is structurally more durable through the forecast period.

The segmentation structure, player benchmarking, and competitive dynamics behind these trends are mapped in the India Buy Now Pay Later Industry by Ken Research, covering end-user sector, channel, business model, consumer demographics, and distribution model segmentation through the forecast period.

India BNPL Market Segmentation: By Sector, Channel, Demographics, and Business Model

The India BNPL industry segments across end-user sector, channel, consumer demographics, and business model - each dimension revealing different growth rates and competitive intensity within one of Asia's most dynamic credit markets.

By End-User Sector:

Consumer electronics leads at 34.6% market share, driven by alignment between BNPL instalment structures and handset or appliance ticket sizes - the ideal use case for new-to-credit consumers without credit card access

E-commerce and retail is the largest channel by transaction volume, with Amazon Pay Later and Flipkart Pay Later embedding BNPL at checkout across fashion, electronics, and home categories

Healthcare and wellness is the fastest-growing sector at 25.58% CAGR, as hospitals and clinics integrate instant credit APIs eliminating upfront deposit requirements at admission - a compelling financial inclusion use case for households facing unplanned medical expenses

Travel and entertainment saw a 300% credit demand surge during festive and peak travel seasons, with LazyPay leading this category through travel aggregator partnerships

Education and B2B are emerging segments with ePayLater leading B2B BNPL as the payment model extends beyond consumer retail into institutional and business payments

By Channel:

Online channels dominate and grow fastest, driven by e-commerce integration and the natural fit between app-based BNPL checkout and India's mobile-first consumer base

Offline POS is structurally significant, with Pine Labs projecting INR 50 billion in monthly BNPL transactions - confirming offline BNPL as mainstream at the POS in electronics, fashion, and home retail

By Consumer Demographics:

Gen Z holds 39.4% of users in 2025 at 23.18% CAGR, driven by mobile-first habits and a strong preference for transparent fixed-instalment structures over revolving credit card debt

Millennials (26-35 years) are the highest-GMV demographic at ~40% of GMV, using BNPL for home upgrades, travel, and consumer durables where instalment structures lower the purchase barrier

Tier II and III city consumers are the fastest-growing geographic segment, consistently outpacing metro demand during festive seasons as digital confidence and BNPL awareness compound

By Business Model:

Fintech-NBFC partnerships are the dominant model, with fintech platforms handling acquisition and UX while regulated NBFC partners provide the lending balance sheet

Bank-embedded BNPL grows at 24.71% CAGR as HDFC, ICICI, Axis, and SBI embed pay-later directly into UPI apps, leveraging low-cost capital and existing relationships to compete without separate acquisition costs

India BNPL Market Competitive Landscape: Pure-Play Fintechs, E-Commerce Giants, and Bank-Led Challengers

The India BNPL competitive landscape has consolidated since 2022-23, with ZestMoney's exit and wallet-linked product discontinuations shrinking the pure-play fintech tier. The market now organises around e-commerce-integrated BNPL, fintech-NBFC partnerships, and bank-embedded credit - each competing on different acquisition channels, risk models, and margin structures.

Key Players in the India BNPL Market

LazyPay (PayU) - Leads by GMV share at approximately 39% of total GMV, competing through e-commerce, travel, and food aggregator partnerships with 300% festive season demand growth and 5 million+ monthly transactions

Simpl - Competes through merchant network depth targeting urban millennials, growing monthly active users and merchants tenfold over 18 months after a USD 40 million Series B; deep checkout penetration is its primary differentiator

Amazon Pay Later (Capital Float) - E-commerce-embedded BNPL within Amazon India's checkout, benefiting from Amazon's customer trust and purchase data with Capital Float as the NBFC lending infrastructure - the most data-rich BNPL product in the consumer electronics and retail segment

Flipkart Pay Later - Proprietary BNPL within the Flipkart ecosystem reducing cart abandonment and increasing average order value for 500+ million registered users

Paytm Postpaid - BNPL accounted for 55% of INR 73.13 billion total loans disbursed in Q2 FY23; Paytm uses BNPL as a credit funnel with 40% of personal loans disbursed to prior BNPL customers

MobiKwik ZIP - Competes through wallet integration, offering BNPL at offline and online checkout to MobiKwik's existing payment user base without requiring a new app

HDFC FlexiPay and ICICI PayLater - Bank-embedded BNPL leaders growing at 24.71% CAGR, leveraging balance sheet strength and UPI integration to offer pay-later at far lower acquisition cost than fintech-only operators

Pine Labs - Dominant offline BNPL infrastructure, enabling INR 50 billion in projected monthly POS transactions across electronics, appliances, and fashion - the primary competitive force in offline channels that digital-only operators cannot efficiently serve

The closely related India Fintech Market, valued at USD 85.13 billion, provides the broader infrastructure context - covering UPI adoption, digital lending platform growth, and the regulatory framework defining the operating boundaries of embedded credit products across the fintech stack.

If you want GMV share by player, end-user sector revenue breakdowns, and Tier II/III city penetration forecasts, download free sample report for a detailed preview.

Conclusion

The India BNPL market at 15.5% CAGR is anchored by consumer electronics and e-commerce volumes, with healthcare the fastest-growing sector, Gen Z driving demographic adoption, and bank-embedded BNPL the fastest-growing model. The competitive landscape has restructured into a concentrated, regulated ecosystem where e-commerce platforms, bank-embedded products, and fintech-NBFC partnerships compete on acquisition cost, underwriting quality, and merchant network depth.

Those tracking BNPL platform strategy, fintech investment, or embedded credit market entry in India will find the India Buy Now Pay Later Industry analysis by Ken Research provides the segmentation intelligence and competitive benchmarking needed to navigate the market through 2031.

FAQs

Q1. What is the size of the India BNPL market?

The India BNPL market is valued at approximately USD 16.2 billion in 2024, growing at 15.5% CAGR to reach an estimated USD 62.6 billion by 2031. Consumer electronics leads by end-user sector at 34.6% share, Gen Z holds 39.4% of total users, and LazyPay leads by GMV share at approximately 39% among pure-play fintech operators.

Q2. Who are the key players in the India BNPL market?

LazyPay leads by GMV share at ~39%, followed by Amazon Pay Later, Flipkart Pay Later, Simpl, Paytm Postpaid, and MobiKwik ZIP among fintech-NBFC operators. Bank-embedded players including HDFC FlexiPay and ICICI PayLater are growing at 24.71% CAGR. Pine Labs dominates offline BNPL infrastructure while ePayLater leads the B2B BNPL segment.

Q3. What is the fastest-growing segment in the India BNPL market?

Healthcare and wellness at 25.58% CAGR, driven by hospital and clinic integration of instant credit APIs that eliminate upfront deposit requirements. Bank-embedded BNPL is the fastest-growing business model at 24.71% CAGR. Gen Z users are the fastest-growing demographic at 23.18% CAGR, and Tier II and III city consumers are the fastest-growing geographic segment by new user acquisition.

Q4. How has RBI regulation affected the India BNPL competitive landscape?

The 2022 prohibition on loading prepaid wallets with credit lines eliminated wallet-linked BNPL products and accelerated the exit of undercapitalised pure-play fintechs including ZestMoney. The market has reorganised around regulated fintech-NBFC partnerships and bank-embedded BNPL, with the RBI's Digital Lending Directions 2025 consolidating the framework. The regulated structure has reduced competitive fragmentation while creating a more durable, compliance-anchored growth trajectory through 2031.